#18 Going Back to the Drawing Board

Weekly Report: 21st Sep-25th Sep, 2020

AUM vs Advances

Word on the grapevine is that the IPO of Equitas Small Finance Bank is coming very soon.

While revisiting their IPO document, I found this statement,

Equitas is the second largest SFB in terms of asset under management (AUM) and total deposits, behind AU SFB

I know asset management companies (like HDFC Mutual Fund, SBI Mutual Fund) use this term quite frequently, but this was the first time I saw a bank use it. In all cases, they either use “loans” or “advances”.

Quite surprisingly, there’s sparse literature available on this concept (In fact, I learnt about it only through a webinar last week).

So I had to share it with you guys. It’s quite interesting.

Since AU Small Finance Bank has the largest AUM, let us look at its balance sheet.

As you might expect, the balance sheet is very clear. There’s no mention of AUM and you see the advances clearly - ₹26,992 Cr

However, from the same annual report, almost all advances were labelled as AUM. In fact, here’s an excerpt:

So if the total AUM is ₹30893 Cr and the advances is ₹26,992 Cr, what is the ₹3,901 Cr difference all about?

To understand this, we need to go back to the basics - Priority Sector Lending. I’ve talked about it quite a lot previously (here and here), but here’s a recap:

There are certain sectors in India, which often gets neglected by banks, so RBI wants it to prioritise them, hence the name. Scheduled commercial banks have a PSL target of 40% of their total loan book. Small finance banks have it way higher, at 75%.

Meeting PSL targets are tough. Not all banks are operationally equipped to meet it. So there’s generally an agreement between banks.

Let’s assume HDFC Bank failed to meet its target for this year. It is around ₹4,000 Cr short of hitting that 40% mark. In this case, it will buy these assets from banks which have exceeded their PSL targets (in our example, let’s assume AU SFB has overshot its target of 75%).

Any excess PSL advance (loan) gets termed as AUM.

Why? Because the selling bank (think AU SFB) continues to service the loan (collect interest payments, provide statements) but it goes off their balance sheet (hence you only see advances there) because they have sold off the legal liability attached with it - essentially, if the loan defaults, that’s on the buyer (think HDFC), albeit with certain conditions.

If you think this is a unique case, think again. It’s fairly common. Here’s a headline from last year:

From the same source, here’s an excerpt:

PSBs and private banks are major buyers and sellers of PSLCs (excess PSL loans); however, if buying and selling is netted, private banks and foreign bankers emerge as major buyers and PSBs, rural regional banks, and small finance banks as major sellers, said the RBI.

This is why you don’t see the AUM term in the annual reports of major scheduled banks, but mostly in small finance banks.

There you go! Once the IPO hits, you can show off this knowledge and appear a bit smarter than your friends!

P.S. Do you want a deep-dive on the small finance bank sector before the Esaf SFB and Equitas SFB hits the market? Like this post and leave a comment so that I can gauge the feedback!

What’s up with RBI?

RBI is on a sprint to push banks towards more tech adoption.

After last week’s circular on NPA automation, the major notification this time revolves around prudent risk management.

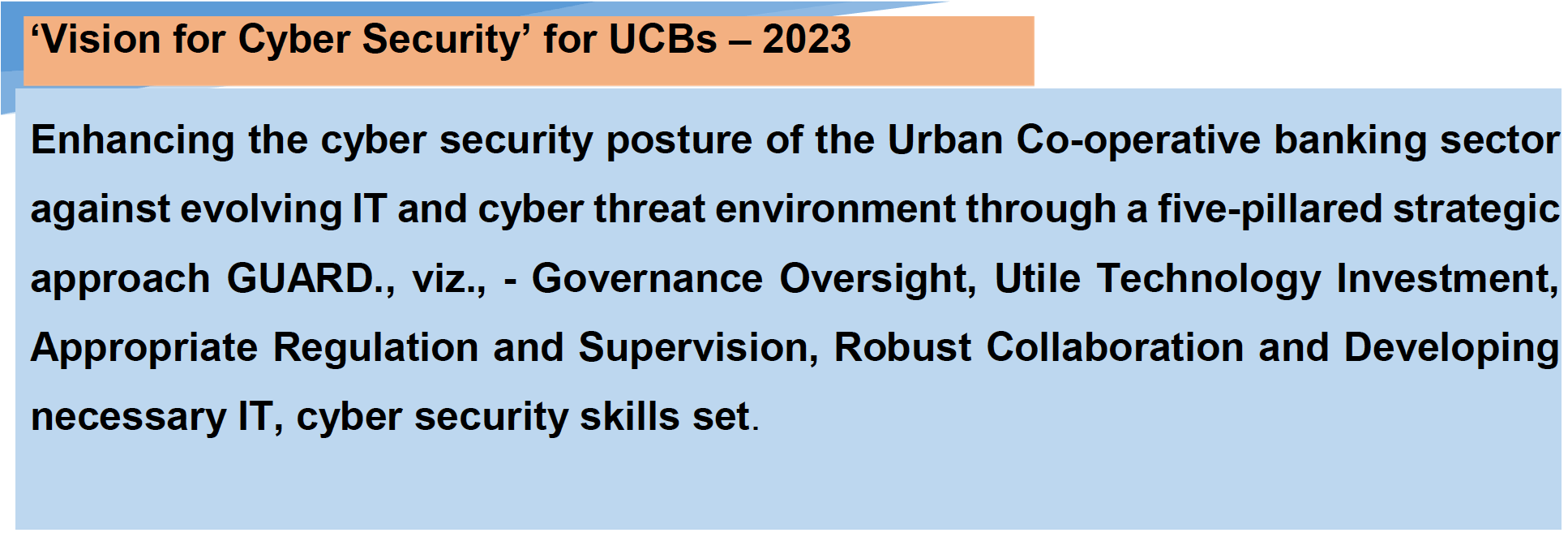

Back in 2018, RBI wanted Urban Co-operative Banks (UCBs) to adopt a basic cyber security framework. Of course, a lot has changed since then.

More co-op banks are offering digital services (mostly payments) which makes it necessary for their security controls to be as sophistical as scheduled commercial banks (think HDFC, SBI).

Rajya Sabha has cleared the Banking Regulation (Amendment) Bill 2020 which brings 1482 such banks under the supervision of RBI (earlier, they were mostly regulated by state governments).

This is like when you have a baby and you want to get all the best things for him/her. Same way, the central bank would obviously want them at par with other big banks. In light of this, it released an updated policy document which a proper vision and all:

Among other things, it wants UCBs to create a reserve/fund earmarked for implementing IT/ cyber security projects. This reserve may be created out of its annual net profits over a period of time.

But this is something that is just not top priority for them.

In our Finance Minister’s own words,

“The financial status of 277 urban cooperative banks is weak; 105 cooperative banks are unable to meet the minimum regulatory capital requirement and 47 banks have net worth in negative,” Sitharaman said. As many as 328 UCBs have gross non-performing asset (NPA) of more than 15%, she added.

The Covid-19 pandemic has hit most of them much harder than the commercial banks. Over the past 20 years, 430 cooperative banks were de-licenced and were forced to liquidate. So will profits go towards maintaining their capital or towards cyber-security?

In such a situation, maybe RBI should buy the newborn a different set of toys?

P.S. If you want to read more on UCB’s background, this article does a good job (written just before the Banking Regulation Bill 2020).

Give me some videsi drama

Whenever I’ve talked about neobanks, challenger banks or any other fintech in this section, I’ve tried to highlight how they do things differently than their traditional counterparts that makes them succeed.

But what is the bear case (pessimistic) for fintech companies?

Think about the business model for once. Neobanks were trying to do everything that the big banks wouldn’t/couldn’t:

Acquire customers through digital channels and millennial-friendly marketing

Eliminated fees (they could absorb these costs because of their funding)

Attracted customers by offering high savings rate

Let’s break down each of these points to understand why they don’t offer a competitive advantage anymore:

If you read the videsi section of my last post, big banks (like Goldman, Wells Fargo, Credit Suisse) are increasingly adopting digital channels to acquire customers at a rate at par with neobanks

Venture-capital backed funding for neobanks have completely dried up. Popular ones such as Monzo and Starling have been forced to bring back fees to appease their investors

According to the Federal Reserve’s latest statement, the policy rate is going to hover around 0-0.25% for a really long time. In this economic environment, how do neobanks offer a high savings rate consistently? (That would be borrowing at a higher rate than you can lend - doesn’t make sense, right?)

I think this chart explains the dilemma beautifully. As you can see, most neobank features only help in customer acquisition, but doesn’t really bring any $ for the company.

Most of this boils down to lack of product differentiation. If as a neobank, all you can offer is slight improvements (like a checking account with a fancy debit card) over the traditional layer, how will your unit economics work?

Either you charge fees, launch completely new products or enable subscriptions (like Jiko or Monzo Plus).

I will talk about all the different types of fintech product offerings in an upcoming post, but broadly there are two ways - payments and lending.

Lending:

Not every fintech can lend as prudently as the big banks - In fact, it was because of Monzo’s bad lending practices that led to its reduced valuation at the beginning of the lockdown. Neobanks in Europe have suffered the most (read here and here). Also, as per BIS, fintech and big tech credit (think Ant Group, Baidu, Tencent) was only around ~1% of the overall credit. Even within this, big tech credit was double than that of small fintech players.

Payments:

When it comes to payments, American fintech players do a better job. Take Chime for example. It is now worth a whopping $14.5B. The company mostly makes money when you swipe their card at merchant places. (You can read their business model here). But this model only works when you have a huge volume of transactions to process. Thus even Chime has other offerings. Its valuation reflects the market it has cornered for itself. How will other players provide an increment advantage over this?

TLDR: The law of innovation applies to everyone, whether you’re an old dog or an overexcited puppy. Fancy websites and cards won’t cut it anymore. Neobanks either need to go back to the basics, stick to their core offering (or change their business model), ruthlessly cut costs or merge with peers. As we move into 2021, we’ll know who were the smart ones anyway.

Long Reads of the Week

International

The FinCEN Files: A year-long investigation by BuzzFeed News and the International Consortium of Investigative Journalists (ICIJ) led to the release of the these blockbuster files. It revolves around a specific term - SAR (or Suspicious Activity Reports). Most major US banks have been named in the list, including Indian ones. To be clear, just because a transaction is “suspicious” does not mean it is fraud. All banks report it. But the way banks delay that and the close ties to dirty money are the real concern here. If you don’t have time for the full report, here’s a summary.

National

Raghuram Rajan, former Governor of RBI, teamed up with Viral Acharya (former Deputy Governor) to publish a paper that outlines all the things wrong with the Indian banking sector and some solutions as well. Although it’s 35 pages long, I really recommend reading it in its entirety rather than some half-baked summary from the news. I would have simplified it here but I found the language fairly simple and not verbose (as I was expecting it to be, since both of them are economists). I do not agree with all the suggestions in the paper but it is still an excellent starting point to “think” how to approach the problem. Enjoy!

That’s it for this week.

If you want me to cover a particular news, want to get featured, write a guest post or simply say hi, reach out to me at anirudha@bankonbasak.com

P.S. You can also connect with me on LinkedIN, Twitter (these are two places where I post whatever that interests me) or on Quora (where I try to help people with their queries related to the banking sector).

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. Since the author is employed by a bank, he has consciously chosen not to report any news related to his company to avoid conflicts of interest. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine, thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action.

Love the way you explain in simple words.

Well Written ..thanks...