#19 Frauds 101

Weekly Report: 28th Sep-2nd Oct, 2020

Welcome to all the new readers who joined this week. We are a now a community of over 2000! 😁 I still can’t believe that such a niche area grew so fast in less than four months. It has all been possible because of your support and feedback.

Keep reading, keep sharing! ❤️

Also, if you’re a subscriber, I would love to hear your thoughts!

Tell me one thing that you love or have learnt from this publication, or simply ANY feedback that you have - comment/reply to this post, it would mean a lot to me! :)

The Tale of Two Lakshmis

In Hindu mythology, “Lakshmi” is a popular Goddess, representing wealth and purity.

Unfortunately, two banks who use this moniker are definitely lacking both.

Here’s two stories from this week, only a few days apart.

Finshots Markets (a financial newsletter, part of Zerodha) explained the crisis at Lakshmi Vilas Bank quite well. You should read it. Even I covered some of their problems three months ago here.

However, I was quite surprised with a similar incident at Dhanlaxmi Bank. On probing further, I realised the two banks shared a LOT more in common apart from shareholders voting out the top management.

For starters, both banks are really old. They were founded just a year apart (1926 and 1927) with seven employees/founders. This is not a trivial point. It is important to understand that both their origins started as a local community bank in South India. As it happens, their ambitions grew bigger than themselves.

Old generation banks have a huge expertise and familiarity in their local communities. As soon as they receive a banking license and try to establish a pan-India presence, they tend to lack management bandwidth (true in both cases). For instance, around 2010, both banks tried to push for growth by extending loans to questionable corporates and risky sectors. This is mostly the result of one overconfident executive (PR Somasundaram for LVB and Amitabh Chaturvedi for Dhanlaxmi)

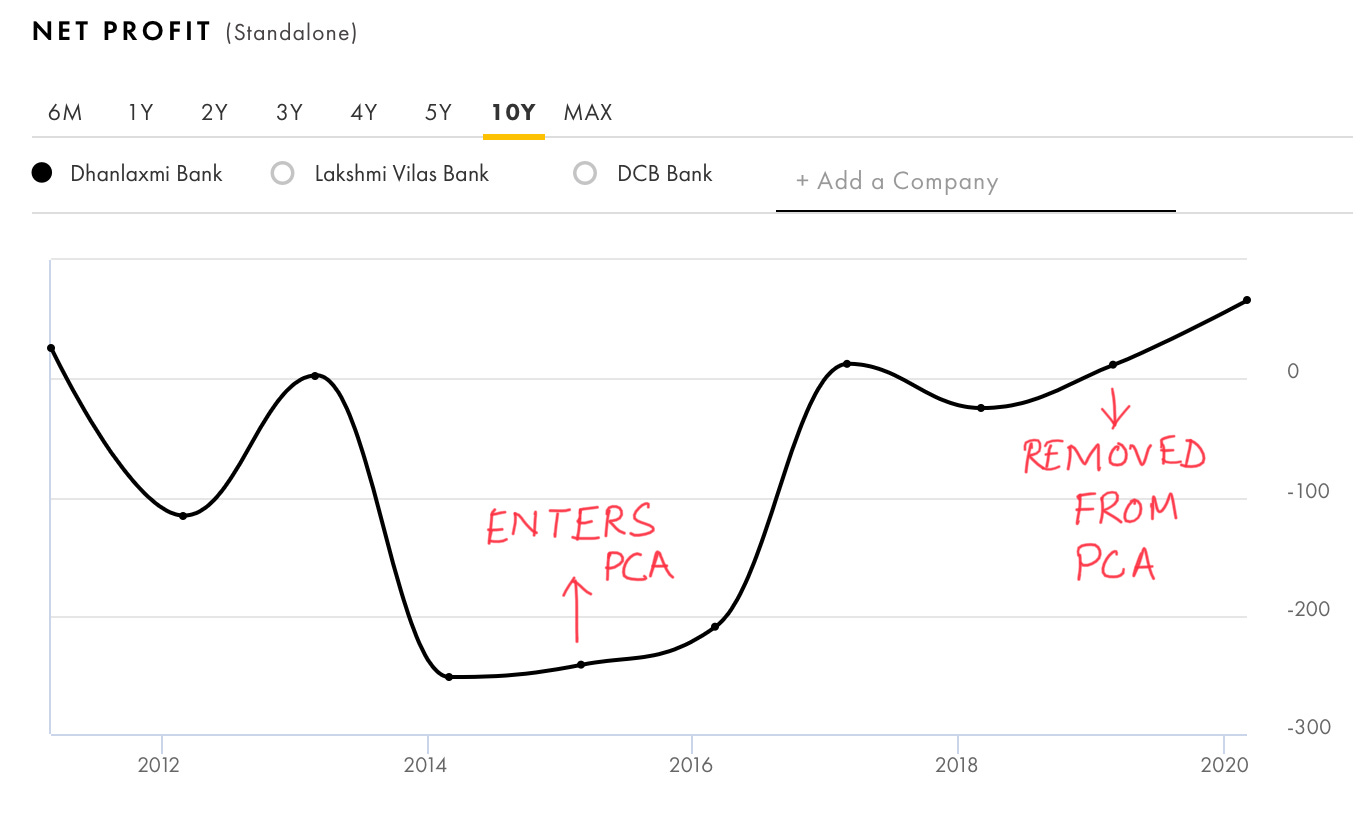

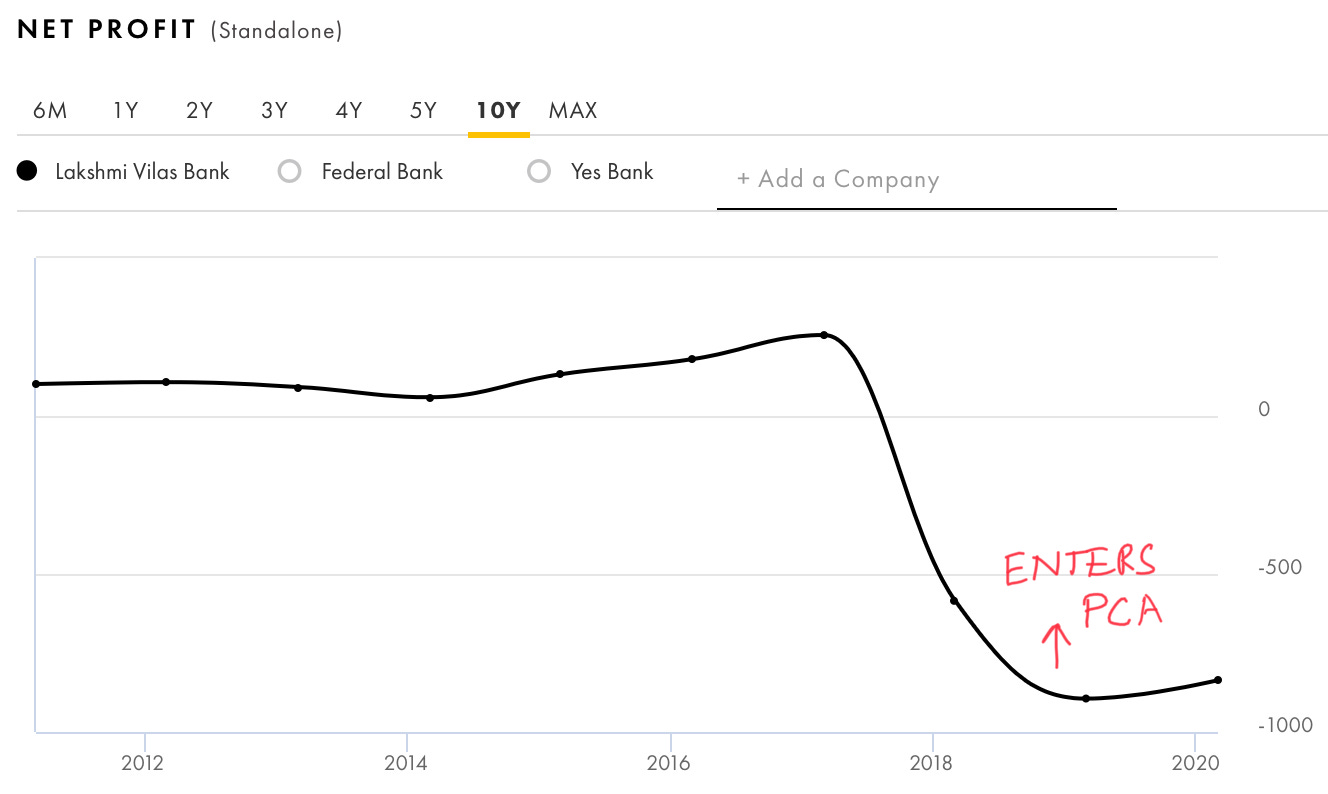

When you take too many risky loans, you also invite huge NPAs. RBI obviously, will notice. Both banks were placed in PCA (Prompt Corrective Action) by the central bank - an action which essentially puts a LOT of restrictions on the functioning of a bank - to prevent it from further mishaps. Although Dhanlaxmi did manage to come out of it, LVB is still stuck in limbo.

(Dhanlaxmi Bank Net Profits over a 10Y period)

(Lakshmi Vilas Bank Net Profits over a 10Y period)

What’s the solution?

If only real life was as easy as exam questions. But looking at the big picture, it seems there are two major ways in which this can be improved:

RBI seriously needs to step up: The management that was voted out by shareholders this week had received clearance from RBI in both the banks. So why did the shareholders not like them? Clearly, the central bank is disconnected with all the stakeholders involved. Since these banks were put under PCA by RBI itself, they should be monitored closely even AFTER the PCA restrictions are uplifted.

Old banks need to stick to their roots or get acquired: Unlike big banks, small banks find it tough to raise money from the market (because they generally lack a strong big promoter). Without money, they can’t grow. If they can't grow, they should just stick to being a community bank or get merged with a large bank which does not have expertise in the area in which the small bank operates. Win-win.

Like I promised, Bank on Basak will try to highlight the strategies and context beyond the news that you read in everyday media. I hope this clarified a lot of doubts that were emerging due to these similar, related incidents.

What’s up with RBI?

Fraud continues to be top priority for the central bank.

Believe it or not, our financial “payment” systems are one of the most sophisticated ones in the world. Thus, it is imperative that strict controls be implemented in order to curb it.

In fact, after sports stars, RBI has roped in actor Amitabh Bachchan for its customer safety awareness campaign.

Two recent safety measures which have been announced are:

Positive Pay System

Applies only to cheques, this system requires the customer to re-confirm certain key details of the cheque (like the date, beneficiary, amount) through SMS, ATM or Internet Banking.

Balancing control and ease of convenience is always a challenge, thus for now, RBI has kept this feature optional for amounts above ₹50,000 and mandatory above ₹5,00,000.

NPCI will build this feature, scheduled to go live from next year.

Debit, credit card rules (IMPORTANT)

New rules for these have already kicked in from Oct 1, 2020.

These measures are meant to empower users to have greater control over their cards.

Any new cards issued/re-issued from this date onwards will only be enabled for ATM/POS usage in India. You will have to put in a special request to enable usage for international usage. (Earlier, this was done automatically with issuance)

If you have never used your card for online transactions in India or abroad, your bank or credit card company will disable this feature.

You can opt-in/opt-out or change transaction limits for your card anytime from your Internet/Mobile Banking option.

You can also disable the NFC (near-field communication) feature so that contactless payments are not prone to misuse.

These new rules are certainly welcome. My only wish is that banks, on their end, make it extremely easy for the user to control these limits right from their mobile. If in 2020, we are required to visit the bank for ANY of these requests, all efforts of RBI will be pointless.

Give me some videsi drama

Continuing with our theme of frauds, this week, we learn about “spoofing".

If you recall my earlier piece on JP Morgan’s revenue streams, I had highlighted how their trading division was solely responsible for bringing in huge revenues that helped it survive the lockdown with ease.

Now, it seems that that the same division has come back to haunt them. In a record move, JP Morgan is all set to pay the highest fine ($920M) in the history of spoofing cases.

To understand just how big JPMorgan's penalty is...in the last six years, financial institutions have collectively paid over $1 billion for spoofing cases.

I think this graphic from the Financial Times illustrates it perfectly.

But wait… What is spoofing?

To put it simply, it is a technical term used in the derivatives market (just like an equity/stocks market, but for slightly complex instruments, like options and futures) when traders (in this case, JP Morgan) put artificial orders in the system to trick market participants (other small traders).

For example, suppose JP Morgan wants to sell silver future contracts. (a financial instrument based on actual silver prices). It puts in an order to sell 5 contracts at 10$. Then it also puts in 100 buy orders slightly below its own sell price, say $9.95. What this effectively does is create an impression that there is a huge demand in the market (100 buy orders vs just 5 sell orders, remember?). So other small retail traders like you and I will obviously think about grabbing this momentum and place buy orders too. Meanwhile, within a few microseconds, JP Morgan removes its 100 buy orders, allowing it to sell its desired 5 contracts to others by falsely creating a demand.

This is bizarre and quite honestly, illegal.

Amazingly, this is not the first time the US bank has been accused of manipulating markets. In 2015, it had paid a $550M fine to the Justice Department for foreign exchange manipulation.

I somehow really like Jamie Dimon, the man running the bank for 15 years. So it’s kind of disappointing that these things keep happening under his leadership. For the largest bank in US, it really needs to step up to prevent frauds like these in the future.

What else happened this week?

International

Each week, I try to highlight racial and gender discrimination in banking. This is yet another case of a major publication goofing up. Her name is Stephanie Cohen, not “Female Banker”, come on! Let’s ignore the sexist author for once, and focus on the positive: Stephanie is now the co-head of the consumer and wealth division at Goldman Sachs (worth $2T). Best part? She might be a potential successor to current CEO David Solomon. Fingers crossed!

If you look at the stock price chart of HSBC (below), the price is back to the same levels at which it listed in the market 25 years ago! What happened to the global bank? Marc’s detailed explanation on his Substack offers a good insight on how banks have become increasingly complex. HSBC, unfortunately, was on the wrong side of it. Read here.

National

Punjab National Bank reports yet another fraud (remember Nirav Modi?). This time, it’s Sintex Industries. To be fair, this is not as outrageous as the Modi scam and looks more like a company defaulting on payments; however, one does wonder about the risk management practices of the bank considering it has the highest exposure among all other banks which lent money. So “fraud” in this context is mostly technical, which means the bank does not expect Sintex to ever return the money and PNB would have to set aside 100% of the exposure from it’s pool of profits (if it does not have profits for the year, it will come out of the capital)

That’s it for this week.

If you want me to cover a particular news, want to get featured, write a guest post or simply say hi, reach out to me at anirudha@bankonbasak.com

P.S. You can also connect with me on LinkedIN, Twitter (these are two places where I post whatever that interests me) or on Quora (where I try to help people with their queries related to the banking sector).

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. Since the author is employed by a bank, he has consciously chosen not to report any news related to his company to avoid conflicts of interest. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine, thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action.

Thank Anirudha Basak sir, for these great posts. It really helps a lot to get information about the banking sector.

Dear Anirudha.. Thanks for interesting post.. Can you please share your views on Marc post of "End of Banking" ...do you think banking industry is really disrupted...