#3 Is RBI finally learning? (8th-12th June)

Cover Story: Payments Banks in India

Author’s note:

I have added a new section “Still want more?” for people who just can’t get enough of banking content! 😁

I’m consciously adding more pictures (trying to design some of them myself) to benefit readers who love visuals! I’ve even collaborated with an Instagram page (Finlad) for this very purpose, because honestly, they do it much better!

The reading time of this article is approximately 11 minutes.

The Rise of Payments Banks

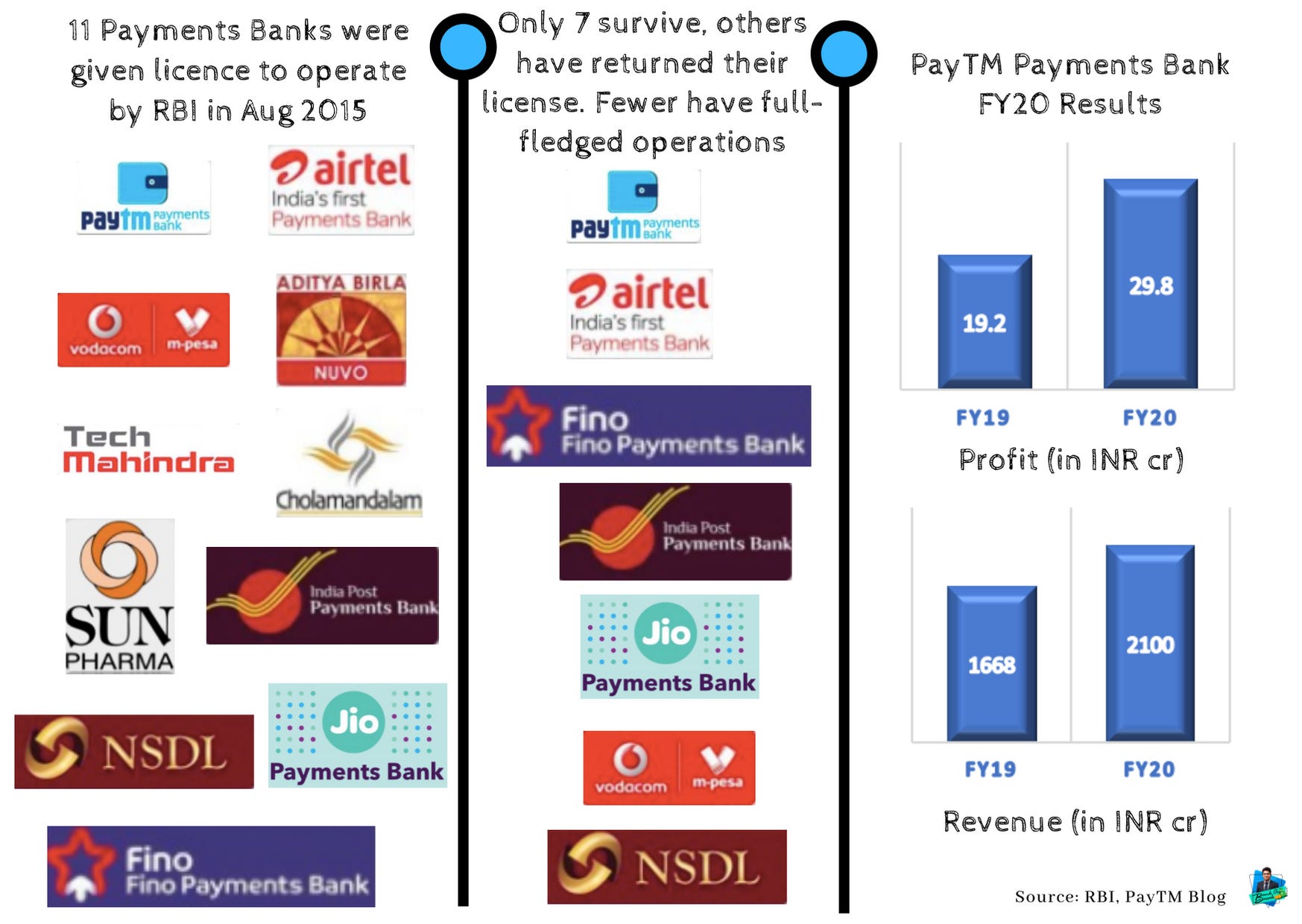

PayTM Payments Bank just released it’s FY20 results. Profits of 30cr over a revenue base of 2100cr. That’s a lot. At a time when other payments banks are reporting losses, how is this kid clocking profits for the 2nd consecutive year?

But let’s back up. What are Payments Banks?

The rules are simple.

What can they do?

They can accept deposits (but only upto 1 lac)

They can issue debit/ATM cards.

They can open savings and current accounts.

What they can’t:

Give you loans.

Issue a credit card.

Well, there are a bunch of other rules as well, but this is broadly it. For the purposes of this article, we need to answer two important questions now:

Why do we need them?

If they can’t lend, how are they making money?

1. The banking scenario was abysmal pre-2014. Look at the figures from a BIS paper:

So what changed? Mostly, the Pradhan Mantri Jan Dhan Yojana.

Under this scheme, 15 million bank accounts were opened on inauguration day. The Guinness Book of World Records recognized this achievement, stating: "The most bank accounts opened in one week as a part of the financial inclusion campaign is 18,096,130 and was achieved by the Government of India from August 23 to 29, 2014"

But there was a problem. Despite the RRBs (Regional Rural Banks), SFBs (Small Finance Banks), LABs (Local Area Banks), there were still some remote areas where it was just not feasible to set up banks. Soon, people were realizing that more people had mobile phones than bank accounts. A bank in a phone, perhaps?

So in 2015, after following the recommendation by a committee headed by Nachiket Mor, RBI finally released a list.

2. Now that you know why they exist, how are they making money? The most basic way a bank makes money is offer deposits at a low rate, lend that money to others at a higher rate and pocket the difference. But payment banks can’t lend, remember?

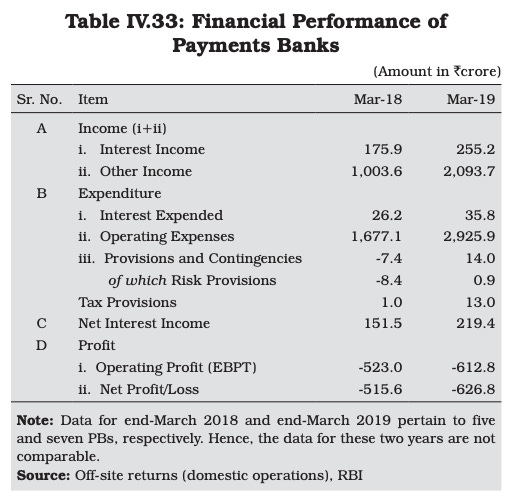

This is precisely the reason why a lot of payment banks folded up. RBI themselves reported late last year that all of them together had an aggregate loss of 626.8 cr.

RBI understood the problem. So in December last year, RBI thought “Wait a second. These small finance banks are doing pretty well. They can lend too! Why not allow these poor souls to convert themselves after a few years?” And they did just that.

But wait. If all of them are making losses, how are some (PayTM and Fino) making profits?

Referring the graphic above, we outline the fate of each of them:

Vodafone M-Pesa: This story ended before it even started. As of January 2020, RBI has cancelled their license, courtesy a voluntary surrender (Reason? Huge losses)

NSDL Jiffy: This guy hasn’t even started properly. Even though it received approval to start operations in Oct 2018, we’re only now hearing that it is gearing up for the ride. This was Sep 2019. The rabbit will wait for the tortoise.

Airtel Payments Bank: Ironically, India’s first PB is still in losses. I guess they couldn’t capitalise on the first-mover advantage. But due to strong backing from the parent (they raised 225 cr from Bharti group this year), it is still chugging along. In fact, it has been really busy this year.

It launched Aadhar-enabled Payment System (AePS). Meaning? Customers of any bank with Aadhaar-linked bank accounts can make financial transactions at the designated banking points of Airtel Payments Bank.

It recently partnered with Western Union to launch real-time cross-border money movement in India and Africa. Airtel is expecting to launch this service by 2020 end.

It has partnered with Mastercard to develop customized products catering to the underbanked spectrum including farmers, SMEs & retail, including solutions for contact-less payments via NFC (Near Field Communication)

With Bharti AXA, it is offering COVID-19 focused insurance plans.

To top it all, 70% of its new accounts have been in the rural area, true to the spirit of financial inclusion. It currently has 30 million accounts. As of last year, its losses were more than the revenue.

Jio Payments Bank: This is again, a relatively new player (since April 2018). So it is yet to make news, but just read this recent interview by the CEO. It clearly shows the amount of clarity that they have and the fact that they’re patient and in it for the long haul. With a Goliath as a parent, it can afford to to be so. My bet? It will be a Dark Knight Rising kind of situation. With SBI as the banking partner, reach is NOT a concern.

Fino Payment Bank: This is the only guy apart from PayTM to report profits this year, albeit it did not disclose the quantum. It only announced a revenue of 689 cr. That’s one-third of PayTM’s revenues. So what’s working for the company? Domestic remittances for one. (transferring money from urban to rural counterparts) - It has contributed 40% of the revenue. Micro-ATM and AePS contributed over 30%. An aggressive phygital (physical + digital) approach, backed by strong parents (BPCL, Blackstone, IFC, LIC, ICICI) made the company learn from the best in reducing costs. They’re notoriously bad in disclosures though.

IPPB (India Post Payments Bank): Speaking of disclosures, IPPB, being owned 100% by the Government of India, is the only PB with a proper annual report. This picture from that document works wonders in explaining the skewed business model of Payments Banks:

IPPB is special in a lot of ways. For starters, no can beat them in the vast network they have of post office branches across the country. This has helped more so during the lockdown, where it has been a blessing in rural areas. How? A person in need of dire cash calls the post office; they send a postman who punches in the Aadhar card details and hands over the cash immediately - Doorstep Banking 101! Can you beat that?

And the best part? Being owned by the GoI, it is in no hurry to show profits.

PayTM Payment Bank: Finally, we come to the beast. Although they haven’t really talked about how they’re making money (nobody does honestly), we can make a few guesses.

It had a huge captive base already from its wallet users.

Having partnered with IndusInd Bank, it could offer deposit rates as high as 7%.

It lured customers in through cashbacks (these losses could be easily shown under PayTM to make the PB’s losses appear minuscule)

Finally, we cannot ignore the massive fiasco it created in the beginning by sneaking in the consent to open a PB while people thought they were doing their KYC for the wallet. If you are an old PayTM user like me, chances are, your payment bank with them is either running or suspended (if its suspended, it means you DID give your consent without knowing at one point)

Business model: By now, we understand Payment Banks have limited scope of revenue. From the deposits they collect, they mandatorily have to invest 75% in Government securities and 25% with other banks. ALL of them do this. So there’s no difference here. The distinguishable factor comes in the form of fee income (through the transactions). Fee income grows with scale.

So the number of customers matter.

Your cost structure matters. Because when you have limited revenue streams, how cost-effectively you onboard incremental customers gives you the edge.

I end with a quick snapshot of all the surviving PBs. I’ll be tracking this space for sure.

IndusInd Bank wants the Kotak Bank attention!

Readers of Bank on Basak know what’s been going on with Kotak Bank. In our last post, we had explained in detail how much Uday Kotak (the promoter) could hold in his own bank.

Super short recap: RBI allows promoters to hold 15% at max. Uday holds ~26%. (although he can cast his votes in the company as if he held only 15%).

How much do promoters of the IndusInd Bank hold? 14.34% as of March, 2020. Wait, that’s within the limit. What’s the issue?

Well, the promoters aren’t too happy that Uday is being treated as the blue-eyed boy while they’re given a step-motherly treatment. And why should they? They’re the richest men in UK!

This is what happens when you set precedent.

I had warned about this. IndusInd Bank is well within it’s rights to demand that the stake limit be raised to 26%. RBI is supposed to observe each case on merit. But can they deny? What if the Hindujas decide to take it up to the court as well? Money sure isn’t a concern for them.

I’ll keep you posted.

In the following section, we understand how RBI is trying to fix these mistakes.

What’s up with RBI?

RBI released a discussion paper on “Governance in Commercial Banks in India”. It’s a 74 page document. I read it, so you don’t have to.

Before I begin, it is important to understand two key things for a bank’s stability/success:

Management

Risk Controls/Processes

Think about it. It is the top management that decides whom to lend, how to borrow. Their aggressiveness or conservatism determines how fast the bank is growing and more importantly, if that growth is on the back of logic or win-at-any-cost mentality.

Risk Controls determine the underwriting standards. What does that mean? These are guidelines set by the banks themselves for determining whether a borrower is worthy of credit. Imagine you turn up at the bank for a loan. They will have an internal mechanism to check your history. Some will check only quantitative measures, like your credit score. Some go beyond, to check qualitative factors as well, like how likely are you to pay back the money? These internal score/points are proprietary and heavily guarded, because they often make or break a bank.

Now that you understand these things, you’ll appreciate the document more. Because the bulk of it is basically how the board should be independent, importance of a Chief Risk Officer, Chief Compliance Officer and so on.

But the important stuff is here:

CEO or WTD (whole-time director must retire by the age of 70)

Any promoter/major shareholder not to continue as CEO for >10 years

Non-promoter CEOs can stay in office for 15 years, but must compulsorily take a break from anything related to banking for 3 years before they can be re-appointed again

Once these guidelines are finalized, any CEO already breaching the above limit will have two years to appoint a successor

It does not end here. Exactly one day after releasing this discussion paper, RBI announces that it has formed an Internal Working Group to review ownership guidelines and corporate structure for Indian private sector banks.

Meaning? This Group will serve two purposes broadly:

Provide a uniform regulation for promoter holding to counter all the different rules RBI had when it gave banking licenses at different time periods

Follow this regulation henceforth for all new licenses

Can you connect the dots now? RBI is basically saying it does not want another Yes Bank fiefdom, Kotak Bank fight or a Bandhan Bank dilemma. Critics are claiming,

for every Rana Kapoor (Yes Bank) there is a Uday Kotak (KMB). And for every Chanda Kochhar (ICICI), there is an Aditya Puri (HDFC)

That’s true. But banking is an extremely leveraged entity which holds public deposits of millions of people and thus, is of national importance. Any measure should limit the risk first, instead of praising the clean.

The Internal Working Group will come out with it’s views on 30th September, 2020.

And the discussion paper? Comments/views are invited till 15th July, 2020.

So if you have any, do let the central bank know. They could sure need it.

Give me some videsi drama

No drama today. Pure data.

Have you ever wondered which are the biggest banks in the world?

Is JP Morgan the first name that comes to mind? Why shouldn’t it? He’s one of the men who built America.

But, like almost everything, China rules the roost here.

Image credits: Finlad

The Banker is a platform which has been tracking the biggest banks since 1970. Their site has some wonderful animations to show the change in dominance over the years for the Top 1000 banks. What you see on Wikipedia is the compilation of the Top 100 banks by S&P Global.

Interesting points to note here:

During the 1970s, US banks dominated. European banks dominated the ‘80s

Although Chinese banks creeped in since 2000s, it was not before 2012 onwards did you really notice the “Big Four” fiefdom.

JP Morgan continues to remain the top bank in the US, followed by BoA and Citi.

Our very own State Bank of India is the only Indian bank that appears in the Top 100. ICICI/HDFC doesn’t appear on S&P and is at the very bottom on The Banker.

Now anyone can quote these figures and appear smart. But it’s also important to understand what happens at the backstage.

Accounting differences: World over, there are two major accounting standards that are used - IFRS and GAAP. These publishers report the assets as they are mentioned in the annual reports. They do not adjust it for these differences. If you think that is minor, think again. JP Morgan would’ve ranked two spots higher had it used IFRS instead of GAAP.

The dollar exchange rate: It is common knowledge that the US Dollar is the strongest currency in the world. This is why this list will always have a bias towards American banks. Why? Because all the assets are reported here using USD. So if the currencies fluctuate, for example, due to Brexit and US-China tensions, Dollar becomes stronger, hence the assets become larger.

So now you know.

Still want more?

If you enjoyed my cover story on Payments Banks, here’s a great piece on “Can Neobanks succeed in India?” (Reading time: 11 minutes)

Although this long-read is written from the point of an equity researcher, it still makes for a great weekend read on an often neglected bank - “DCB Bank | The Turnaround Story” (Reading time: 21 minutes)

Professor Ananth Narayan of SPJIMR warns us of a financial train wreck - and how even acknowledging the bad loans (NPAs) in our banking system can go a long way in cleaning them up. (Reading time: 9 minutes)

I’ve deliberately not covered the Supreme Court-RBI-SBI case going on right now since the next hearing is on 17th June, but click here if you want to read a short primer.

I end with this heart-warming video from Axis Bank asking us to #ReverseTheKhata.

That’s a wrap for the week. What did you think? Good, bad, yuck? Let me know in the comments.

If you want to reach out to me for a detailed feedback, want me to cover a particular news, want to get featured, write a guest post or simply say hi, reach out to me at anirudha@bankonbasak.com

In the meantime, tell your friends!

P.S. You can also connect with me on LinkedIN, Twitter (these are two places where I post whatever that interests me) or on Quora (where I try to help people with their queries related to the banking sector).

very well explained Anirudha

Wonderful article with equally wonderful presentation.