Would you believe it if I said that I almost finished writing yet another edition of Bank on Basak filled with news (and context) from the past week?

And then it hit me.

This is the last edition for the year. 🤯

We will NOT get another chance to reflect back on all the things that shaped this industry (for the better or for worse).

So instead of a fresh new piece, why not take a step back and understand the year gone by…

The Year of Moratoriums

This word has been used and misused by banks, lawyers, courts and mostly misunderstood by individuals.

I still remember Aseem Dhru elucidating the problem in his own unique way!

Of course, his argument at the end doesn't make sense anymore, because this issue found its way to the highest court of the country, in which the judgement resulted in waiving off the “interest on interest” on these loans.

I have tried my best to explain the core law revolving around this entire episode here.

Unfortunately, the year is about to end and the matter is still lingering in the Supreme Court.

However, you would be surprised to know that the first major usage of the word “MORATORIUM” was not related to loans this year, but the capping of withdrawal limits on a popular private bank at the beginning of March.

From the notification,

Notice the sections from the press release that I’ve highlighted.

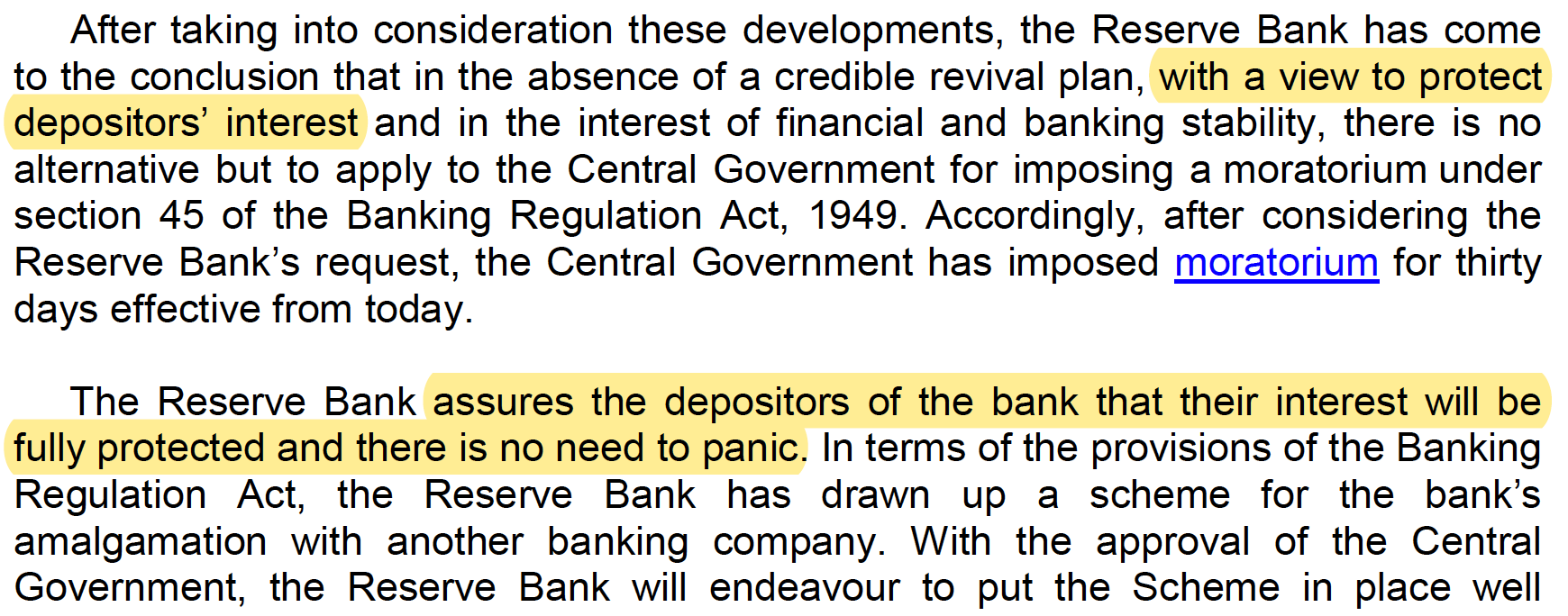

Now, fast forward to November.

From another moratorium of another private bank in India,

Do you notice the uncanny similarity?

These are two distinct events with two wildly different banks spaced almost eight months apart.

However, despite all the differences, it revealed a lot about the regulator and the industry:

RBI still has a long way to go to proactively identify banks which are about to go under…

But, it is also getting better at these amalgamations: From a public money led revival (in the case of Yes Bank) to a foreign bank-led rescue (in the case of LVB)!

It does not matter who you bank with anymore - RBI has made it abundantly clear - as long as it is a scheduled commercial bank, depositors will always come before shareholders and bondholders of a bank!

So going into 2021, like RBI says - don’t panic! :)

The Year of Regulations

RBI has been busy busy busy.

There were weeks when I struggled to find a cover story for the day; but there was never a dearth of content for my “What’s up with RBI?” section.

Honestly, you can complain all you want about the strict rules that our central bank imposes, but you’ve gotta admit how well it has kept everything from falling apart, so much so that some people prefer to call it The Dark Knight.

RBI came all guns blazing at COVID-19, infusing funds totalling 3.2% of GDP into the economy since the February 2020 monetary policy meeting to tackle the liquidity situation.

We learnt so many terms - TLTRO, OMOs, SDLs, WMA - all of which I’ve covered in some form or the other in this newsletter.

In fact, RBI had set up a dedicated webpage where you can find all the announcements that it came out with, solely to target the after-effects of the disruptions related to C-19.

In the midst of all of this, the central bank did not forget its core responsibilities (hint: read the Preamble in the image above):

Regulate the interest rates in the economy despite a flawed objective and rising inflation rates.

Be an effective (?) debt manager for our Government

Also, it didn’t shy away from taking away new responsibilities - taking in co-operative banks under its fold.

Of course, being “busy” did have its perks. Even the US Central Bank is 300,000 followers short of the following milestone:

In 2021, I look forward to 5 things from the regulator:

How RBI is able to tackle the impending doom of NPAs that might possibly come tumbling out of the closet.

Take the FinTech ecosystem further, through the Regulatory Sandbox as well as completing all the goalposts for the Payment Systems Vision 2021

More Consolidation in the Sector (need to remove the bad apples from the ecosystem)

Selecting a worthy competitor to NPCI

Better regulations for NBFCs

2020 was a roller-coaster ride for the banking industry. It’s a special number for me as well.

Although this mail goes out almost 2600 individuals, there are ~2020 of you who regularly open my mail. :)

That means a lot!

It has been a really fun journey to learn and grow with you guys.

That’s it for this week for this week though!

Happy New Year!

..and see you on the other side, trying to understand a little more about this maddening little industry!

Love, Basak.

I love feedback. If you want me to cover a particular news, want to get featured, write a guest post or wanna simply say hi, do reach out to me at anirudha@bankonbasak.com or LinkedIN or Twitter. Meanwhile, like this post and share it around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. Since the author is employed by a bank, he has consciously chosen not to report any news related to his company to avoid conflicts of interest. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine, thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action