#38 The Regional Players...

CSB Bank and Financial Awareness

Hey guys! It’s been a long time since I’ve done a deep-dive on an individual bank. Let’s start with a relatively new one for now.

The Great Turnaround

When I said the bank was new, what I really meant was that the bank was new to the stock markets, having listed on December, 2019. It has been around since 1920 (over 100 years old)!

But that’s not the only reason it calls itself a century “young” organisation.

It has done a couple of things to shed it’s heritage image.

Let’s go for it step by step - if you’ve read my previous deep-dives, you will identify recurring themes in what makes a bank great:

Management

Capital

Workforce

Lending book

Let’s start with the management.

Mr. Rajendran has over 40 years of experience in the banking sector, having been associated Corporation Bank, Andhra Bank and the Bank of Maharashtra. In his last role (before CEO of CSB), he served as the chief executive for AMFI.

Capital

Right after he took up the position, he travelled across the world to meet shareholders, including an influential Bishop (CSB stands for Catholic Syrian Bank) to convince them about allowing a new deep-pocketed shareholder on board (Canadian billionaire Prem Watsa’s Fairfax, which infused ₹1,200Cr for a 51% stake).

This heavy infusion of capital was a miracle for the bank. For multiple years (2009, 2013 and 2015), CSB had turned to its existing shareholders whenever they needed money to grow.

However, post 2015, it ran into losses (of about ₹150Cr) which were severely depleting it’s equity capital. There’s only so much you can borrow from existing shareholders so an outsider at an opportune time really helped.

“For the past 20 years we have been constrained for capital, now we have more than we expected” - Mr. Rajendran after CSB got listed.

Next step: workforce.

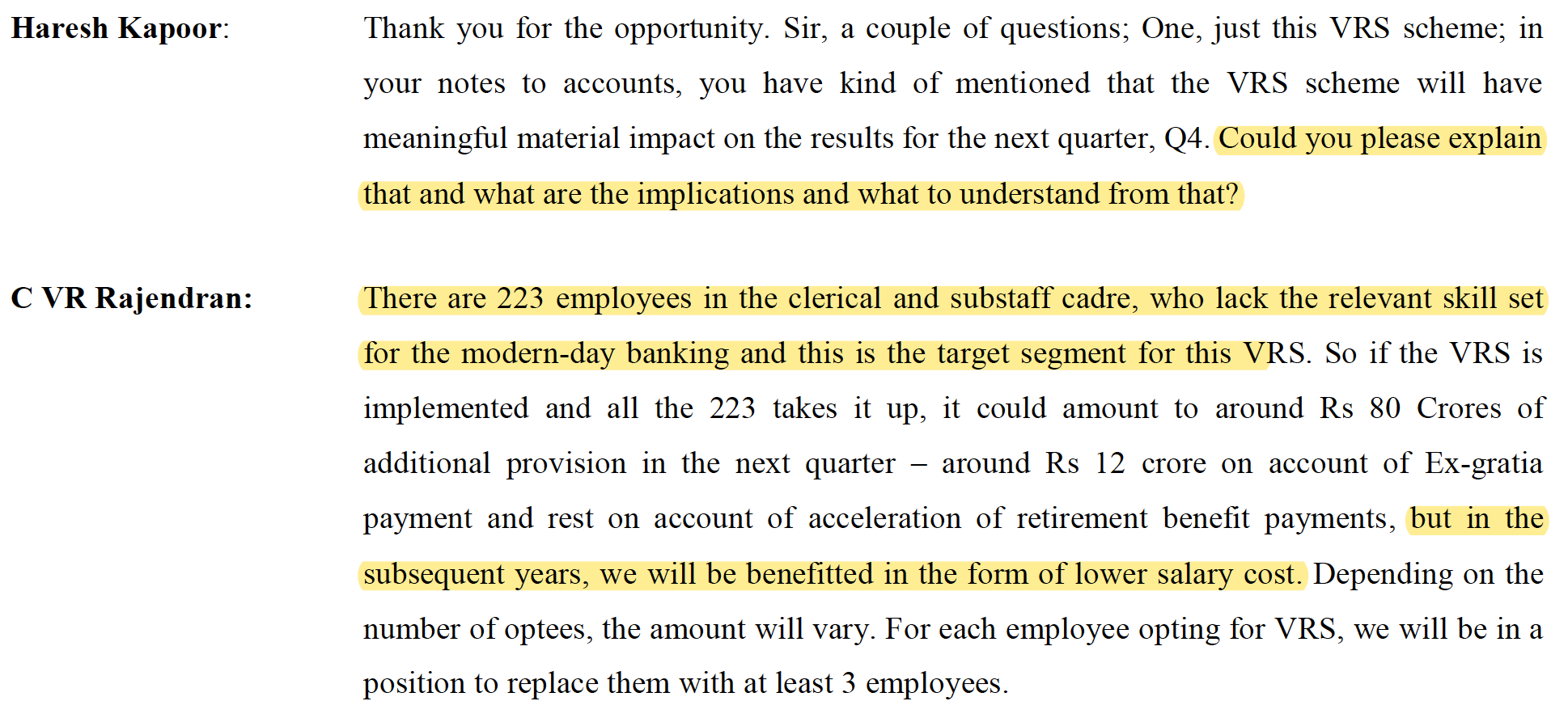

The existing employees had been around for a decade (mostly due to politics) and were untrained. Of course, this impacted branch-level productivity. Mr Rajendran sacked around 200 for underperformance, offered another 1000 VRS (voluntary retirement scheme), reduced the retirement age by two years and recruited fresh young faces. The result? Today, less than 50% of the previous employees are in force and the average age of employees fell from 50 to 36.

Once you look up VRS (if you aren’t aware), you’ll be better able to understand how this move improves overall performance as well as reduces costs for the bank in the long term. Here’s an excerpt from their analyst conference:

Portfolio

From the IPO prospectus, CSB outlines four principal business areas (and their respective shares in the total loan book as on March 31, 2017)

SME Banking (43%)

Retail Banking (44%)

Wholesale Banking (13%)

Treasury Operations

In case you’re wondering what’s included in the last,

“Our treasury operations primarily consist of statutory reserves management, asset liability management, liquidity management, investment and trading of securities, and money market and foreign exchange activities”

Let’s see how they’ve changed since 2017. Here’s an advances break-up from their latest filing:

You can’t really the ignored the red color even if you wanted to. From 24% at the end of 2017, gold has massively reached 40% of the total loan book.

Although RBI’s decision to increase the gold LTV to 90% really helped the bank, the average LTV for all the gold loans in their portfolio stood at 82% as on December 2020.

Explainer: This essentially means that if they hold gold worth ₹100 on their books, they have lent out loans worth ₹82 against them - this is okay as long as the price of gold doesn’t fall drastically - if it does, it won’t be too good for them since almost half their book is only gold loans!

Here’s an excerpt from Mr. Rajendran explaining the importance of gold loans:

This isn’t without its advantages though. Net profit for the last quarter has doubled on a year-on-year basis on the back of this 60% jump in gold loans!

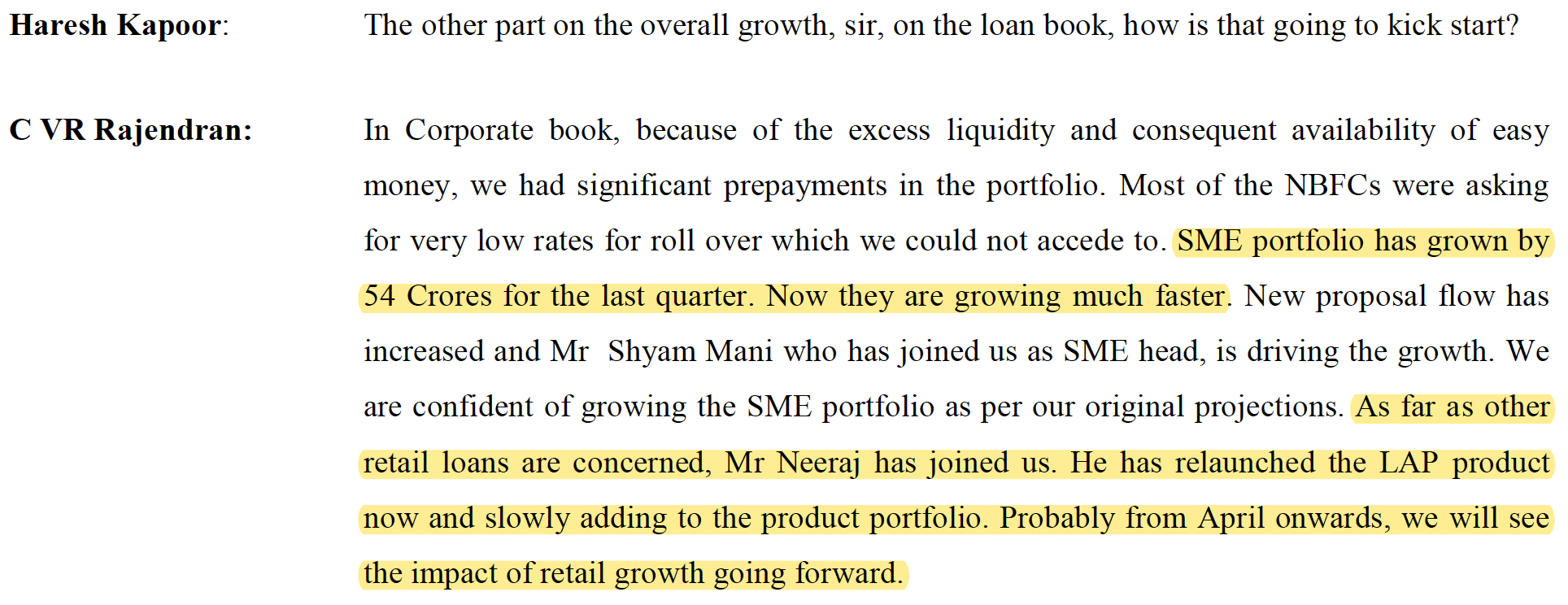

Of course, Mr. Rajendran is cognisant of this over-exposure and he has addressed questions on how to grow the rest of the book. Two important additions in the SME and Retail Segments is expected to drive these segments.

Overall

It has been fun trying to study how a century old institution has been trying to convert itself into a new age lender, to keep up with the times through investments in human capital and technology.

I hope you have learnt something as well - how focusing on a few pillars can really get the job done and I will be keenly following the growth of CSB in the coming years!

What’s up with RBI?

Every year since 2016, RBI has been conducting Financial Literacy Week (FLW) every to propagate financial education messages on a particular theme across the country.

For this year, the theme was: “Credit Discipline and Credit from Formal Institutions”

With all the unbridled proliferation of sketchy loan apps throughout the past year, I guess it makes sense for such a theme.

I could find three TV commercials listed on the RBI website. I don’t watch TV so I don’t know how frequently they are run but I must admit that they do a decent job.

This one talks about the benefits of repaying your EMIs on time - clearly outlining that you’re credit history will remain unaffected and the fact that it’ll be easier to get another loan second time around in the future.

This one talks about the benefits of responsible borrowing - the husband is shown announcing the happy news of being approved for a business expansion loan - the wife asks if they could use the money to buy a new AC and also plan a holiday trip - and the husband basically YOLO agrees to it (what?)

Ofcourse, I couldn’t find data to verify this but if this made into a full-blown TVC, I’m sure a LOT of people do this regularly.

I feel the only ad which they could definitely made a little better is this one:

Here, although the RBI mascot warns the person not to click on suspicious links on his computer (titled “Get Quick Loan Now”) - warning that he may have to pay high interest rates - he could have done a better job explaining where to find a “RBI registered finance company”, considering these customers are the ones who usually get declined by a bank.

Overall, I believe it’s a commendable initiative, which will only get better with time.

A few startups are trying to solve this in their own way (remember, credit discipline and awareness is not correlated with wealth, so this is a pretty universal problem to solve).

Did you know? that the RBI mascot used in the TVC above is a a decade old! His name is MONEY KUMAR (very original lol) and he used to appear in comics to teach monetary policy and caring for your currency to kids.

That’s it for this week.

I love feedback. If you want me to cover a particular news, want to get featured, write a guest post or wanna simply say hi, do reach out to me at anirudha@bankonbasak.com or LinkedIN or Twitter. Meanwhile, like this post and share it around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. Since the author is employed by a bank, he has consciously chosen not to report any news related to his company to avoid conflicts of interest. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine, thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action.