Some of us may have faced a situation where we’ve tried to track down money lying idle in bank accounts, left in the name of a closed one who has passed away.

Or maybe even while they’re alive - banks usually have draconian requests such as asking the elderly to visit the bank for basic stuff such as FD renewals.

In majority of cases, these never get claimed. Where does it go?

As per a RBI regulation dating 2014, banks are supposed to maintain these inoperative and unclaimed accounts for a period of 10 years, post which they need to transfer the entirety (including any accrued interest) to RBI.

RBI maintains these funds in a separate account called the DEA (Depositors’ Education & Awareness) Fund.

In case you’re wondering if this figure is small, RBI actually publishes the data every year in its Annual Report since 2014.

Screenshot from 2021 RBI Annual Report - Page 254

Yup, almost ₹40,000 crore!

For the last three years, roughly ~₹6,000 crore gets added to this fund each year!

Did you know? The fund started with a base corpus of ~2800 crore. In just 8 years, it has seen a 14-fold increase!

Enough of data. Let’s try to answer some important questions now:

How do I know if my family has inoperative/unclaimed accounts?

Banks are supposed to display such information on their websites. Here’s the relevant link for ICICI Bank, where you can search by Name and one other unique identifier. This is actually the first step. Next steps involve the arduous task of visiting the bank and submitting all required documents.

Note: There is no change of procedure on your end if 10 years elapse and the money gets transferred to the RBI. It just might take a little longer for the bank to process such requests.

Do I continue to get interest on forgotten accounts?

Yes! Your forgotten savings account will continue to fetch the same rates that the Bank provides to everyone else. In fact, it will continue to accrue interest even after being transferred to the RBI - in such a case, the interest rate will be determined by the central bank from time to time.

What does the RBI do will all this money?

It invests in government securities - the interest earned is used to pay the interest accrued on these funds and also, as the name suggests, fund various investor awareness initiatives for the benefit of Indian savers.

If you want more specific details, RBI has outlined them here:

One of the biggest mistakes people still do is not informing their close ones about their various savings. The second big mistake is not updating the name and date of birth of the nominee who’s due to receive the funds on your demise. Do both and you’re good to go!

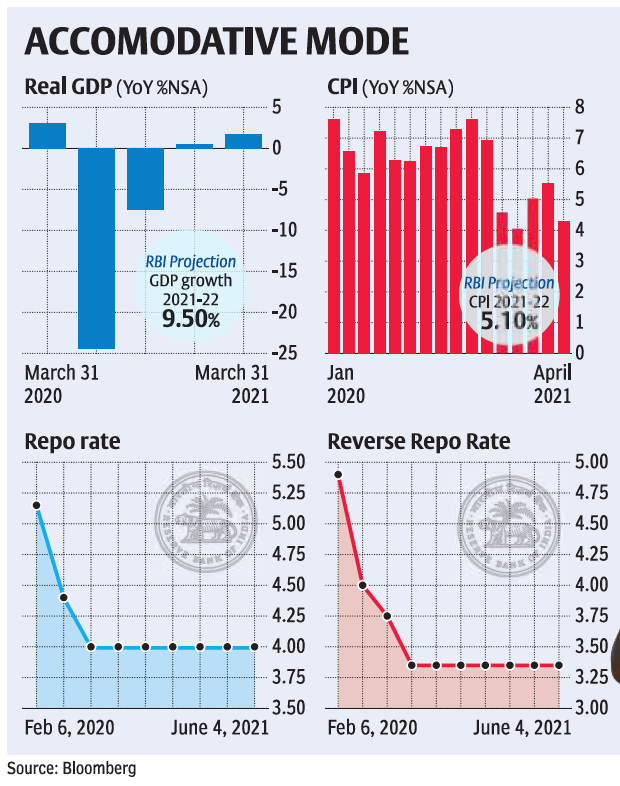

This is where the central bank updates us about any change in repo rates (majorly) and any other announcement it deems fit.

As the repo rate has been largely kept unchanged since the beginning of last year, these meetings mostly gather attention for the stuff that’s announced apart from this:

You can get your salary on weekends too!

Payment of company-wide salaries (or any other bulk transfer for that matter) relies on a payment mechanism called NACH (National Automated Clearing House). After NEFT and RTGS, NACH is also being made operational 24x7 from 1st August, 2021. Now you can even make your EMI and SIP payments over the weekends. As digital payment systems become more ubiquitous across the country, a round-the-clock payment settlement system goes a long way in deepening the ecosystem!

No change in Crypto stance!

“RBI’s position is that we have major concerns around cryptocurrency, which we have conveyed to the government. But the central bank does not give investment advice. It is up to each investor to make their own appraisal and due diligence and take a very careful call on their own investments”

This only came up because RBI asked banks not to reference an out-dated circular if they did not want to deal with crytpo-related payments.

I love feedback. If you want me to cover a particular news, want to get featured, write a guest post or wanna simply say hi, do reach out to me at anirudha@bankonbasak.com or LinkedINor Twitter. Meanwhile, like this post and share it around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine; thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action.