#6 We Survived a Quarter...barely!

Weekly Report: 29th June-3rd July.

Chart of the Day

Image source: BloombergQuint (BQ)

This is a scary chart. By all estimates, the coronavirus will take the banking sector to pre-2000 levels.

Two major CRAs (credit rating agency) - S&P and Fitch, are basically saying the same thing - NPAs are going to rise. Slowly, steadily, but surely.

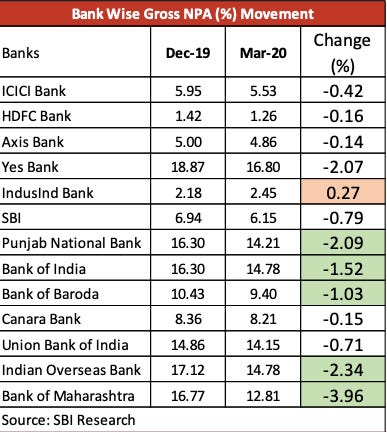

The situation is going to be worse in public sector banks compared to private ones:

Image source: SBI EcoWrap Report, 29th June, 2020

A lot of history is hidden in the BQ chart above, but that’s a story for another day. For now, let’s observe two key inflection points:

2008: Do you notice that the NPA levels were at an all time low? How can that be? Didn’t the global financial crisis occur during that time? Well, you’re right. But the RBI conducted an exercise known as the “restructuring of loan” - basically renegotiating terms with the borrowers so that they did not have to report those pesky NPAs in their balance sheets right away. Ofcourse, our banks always had a tendency to hide the loans as well.

2015: Do you notice the sudden spike after 2015? During that time, RBI conducted the “Asset Quality Review” - think of it as a random check of bank balance sheets by RBI. Lo and behold! All the secrets come tumbling out of the closet and the true picture gets captured!

Skip to June 2020: What’s happening now? With the coronavirus as an excuse, cries of another “one-time restructuring of loans” is being considered by the Government, banks and the RBI.

And the cycle continues. Sigh!

P.S. If you want the Fitch report, hit me up! (contact details at the end)

What’s up with RBI?

Do you remember the Government’s ambitious 20 lac crore package announced on May 13th?

If you don’t, let me refresh your memory. This was one of the announcements made in the first tranche:

Well, this finally came through. RBI released a notification this week explaining all the contours of this deal.

How does it work exactly?

To understand that, we need to identify the problem. To put it very simply,

NBFCs are institutions which lend to those people whom the banks won’t typically lend. BUT they are not allowed to accept deposits from the public like banks. So who do they get the money from? Banks! (because banks find it easier to determine the credit-worthiness of NBFCs rather than small borrowers)

Because of COVID, loan moratorium was allowed and subsequently availed by a lot of borrowers. Since they had stopped paying their EMIs, NBFCs (non-bank lenders) could not repay money to the institutions they borrowed from.

Considering the grim situation, banks also stopped lending fresh money to the NBFCs. So now money ain’t coming in from anywhere, but the NBFC still has to honour the repayments.

Enter the hero: a super complex arrangement, which I’ve tried to simplify with my excellent handwriting: 🙈

Most things in the diagram are self-explanatory. SPV (special purpose vehicle) is just a temporary entity created so that everyone has a one-hand distance from all these deals and aren’t directly affected in case of any fallout. (also for boring regulatory and legal purposes).

Advantages:

The SPV (special purpose vehicle) ensures that the NBFCs meet all of their repayments - at least until the moratorium lifts (on 31st August)

Banks don’t have to declare NPAs as they will get their money back

The arrangement MIGHT be extended after assessing the situation on September

Disadvantages:

This is a temporary measure at best - a solution which solves a short-term problem - new business is not being generated by this, only old ones are being repaid

This scheme might be prone to misuse - there is no measure to check if a particular NBFC actually needs this money

The low-rung NBFCs, which actually need this, might not even qualify for this because of the stringent rules set up by RBI

Give me some videsi drama

The BIS is the most important bank in the world that you’ve almost certainly never heard of - Adam LeBror, author of “Tower of BASEL”

Established in 1930, the Bank of International Settlements was set up mainly to help with transfer payments between countries during the First and Second World War. However, post these wars, it slowly got transformed into an international entity which acts as a common destination for facilitating collaboration among central banks around the world (it boasts having 62 central banks as it’s members)

Did you know? The BIS is headquartered in Basel, Switzerland. The name sound familiar? BASEL I, II and III are the foundations on which central banks determine regulatory requirements for commercial banks.

Among other things, because of it’s wide reach, it has become quite the repository of excellent publications and research papers, like this one, which talks about the lessons that the world can take in from the success of UPI in India.

Today’s topic, however, is the Annual Economic Report 2020, which it published this week. It’s a long read, so I’ll put in a snippet which I found really interesting:

Notice the first chart. The black line demonstrates a +ve or -ve inclination of adopting CBDC (central bank digital currency) by central banks around the world.

With the advent of Bitcoin, Facebook’s Libra and other private digital currencies, the report makes a valid case in the benefit of the central banks themselves adopting this, instead of shunning them away: so that they can act as an operator, catalyst and overseer. This will hopefully foster innovation among other private participants as well.

From the report,

Central banks run or play a key operational role in many such systems, such as TARGET Instant Payment Settlement (TIPS) in the euro area, the Faster Payment System (FPS) in Hong Kong SAR, Cobro Digital (CoDi) in Mexico and PIX in Brazil. In India, the unified payments interface (UPI) was set up with central bank guidance and support.

Obviously central banks want to control the money supply instead of a decentralised entity like Bitcoin. This report just pushes central banks to get one step ahead.

Movers & Shakers

Rajkiran Rai, MD & CEO, of Union Bank of India, who’s tenure was supposed to end on 30th June, 2020 received a two-year extension so that the merger of the bank with Andhra Bank and Corporation Bank gets completed in a smooth manner. It would be unwise to change management during a merger process.

In case you’ve forgotten, our Finance Minister had announced a mega merger of 10 PSBs (public sector banks) into 4 strong PSBs. Although the official mergers have all taken place on 1st April, 2020, the integration process is delayed due to the coronavirus. Here’s a useful chart for the same:

In my #4 post, I had mentioned Pralay Mondal, ex-head of Retail at Axis Bank had jumped ship to Catholic Syrian Bank in a similar role. CNBC reports that role has now been filled by Sumit Bali, who’s last role was of CEO & ED, IIFL Finance. Prior to that, he led Retail at Kotak Mahindra Bank. It’s important to be aware of these changes as Axis Bank is bullish on retail and conservative on wholesale lending.

Image source: Axis Bank Investor Presentation, March 2020

Still want more?

I discovered Nathan Tankus this week, who got profiled by Bloomberg. He’s a 28-yo who hasn’t finished his bachelors’ yet but writes a Substack newsletter on all the policy actions of the Federal Reserve, which he covers so well that he’s followed by the who’s who of the US central bank, the SEC, the OCC as well as the DoT. 🤯

Nathan is an inspiration for many, especially myself, who’s trying to do a similar thing in India. So thank you for reading this all the way till here. Your support means a lot. 😊

For this weekend, read this excellent piece by Nathan which busts the myths on CLOs (collaterized loan obligations).

That’s a wrap for the week. What did you think? Good, bad, yuck? Let me know in the comments.

If you want to reach out to me for a detailed feedback, want me to cover a particular news, want to get featured, write a guest post or simply say hi, reach out to me at bankonbasak@gmail.com

In the meantime, tell your friends!

P.S. You can also connect with me on LinkedIN, Twitter (these are two places where I post whatever that interests me) or on Quora (where I try to help people with their queries related to the banking sector).