#25 Digital Future

Axis Q2, RBI's FinTech concerns and Singapore's digital banks...

Happy Diwali everyone! Based on my social media feed, I kind of felt this was the first proper holiday that India enjoyed since the lockdown. Hope you had a wonderful time as well! :)

The Quiet One

Over the past few weeks, we’ve covered almost every major bank. I think Axis Bank will close the loop, post which I’ll try to find ignored banks again.

Ideally, there’s a lot to cover for the third largest private bank of our country. However, keeping with the theme for this week, we will focus on its digital banking strategy exclusively.

From its latest presentation, here’s a snapshot of all its doing in the space.

Yes, I know, that’s a lot of information packed into one slide.

So let’s break it down. Here’s what stood out from the clutter:

They’re clearly putting in a lot of energy here, with over 100+ dedicated hires and >80% of them from a non-finance background, they want a new set of eyes and talent to grow this division.

Digital products contributed a significant portion of the Bank’s sales with 78% of savings accounts, 75% of FDs, 65% of personal loans, 51% of credit cards and 48% of new mutual funds in Q1 sourced digitally.

As of Q1, they were the 2nd largest remitter as a PSP bank in the UPI ecosystem (partner bank for companies such as Amazon Pay, Credit, GPay, Whatsapp Pay)

A good measure of digital banking adoption is how seamless it is do most of your banking stuff through your mobile, without having to rely on a desktop or laptop for internet banking.

If you remember the lesson from Federal Bank, meaningful tie-ups can go a long way in establishing your digital presence.

After Freecharge and Flipkart, the bank has been able to partner with Google for a new credit card.

Not to be left behind, the bank has finally gone live on the Account Aggregator (AA) platform this month.

“Account aggregators are a set of non-banking financial companies, which work as technology intermediaries between companies seeking financial data of customers (financial information users) and those holding that data (financial information providers).” As of now, Axis Bank falls on the latter spectrum.

It’s too early to comment on the efficacy of AAs. However, being an early adopter would surely help the bank in amassing more customers digitally. (Remember, each new client sourced digitally is a relief on the cost-end, something which the bank hasn’t been able to manage very well - just check the NIM concept in the last post)

Honestly, when I began covering their strategy, I had high hopes, but it leaves the heart yearning for more. Axis is one of the fore-runners in this space, but hasn’t been able to create an impact yet. Let us hope it can change that soon.

What’s up with RBI?

I guess like everyone else, folks at RBI have had a little too much time on their hands working from home as well.

After a seven year break, RBI has started releasing its monthly Bulletin again.

The Bulletin made its first appearance in January 1947. Coupled with the Weekly Statistical Supplement, I believe it has done a fair job in increasing the overall transparency of the system - apart from the constant content material for journalists and bloggers, it also increases accountability and competitiveness.

So what’s special about the Bulletin?

All the Press Releases that make its way to the landing page of RBI are the ones that usually get reproduced in the Bulletin - so be rest assured, if it’s important, I’ve covered them in this newsletter already.

However, there are a few nice articles that only show up in the Bulletin. For example, for this month, we had articles ranging from the state of the economy, a snapshot of household financial savings from Q1, determinants of term premium (the difference in the returns on a long-term and short-term bond) in India, our gilt (government securities) market, LIBOR’s rise and fall (I had simplified this in Edition #12) and finally one article on FinTech.

I’d suggest you go through the entire Bulletin for your article of interest/domain as I’ll only be covering the Fintech article here.

As expected, the article is structured from a perspective of a regulator, how it sees the entire industry emerging and how it needs to keep itself updated with the times.

To best visualise that perspective, here is an excellent infographic to explain how the different FinTechs and their accompanying enablers lie on a solid bedrock of regulations.

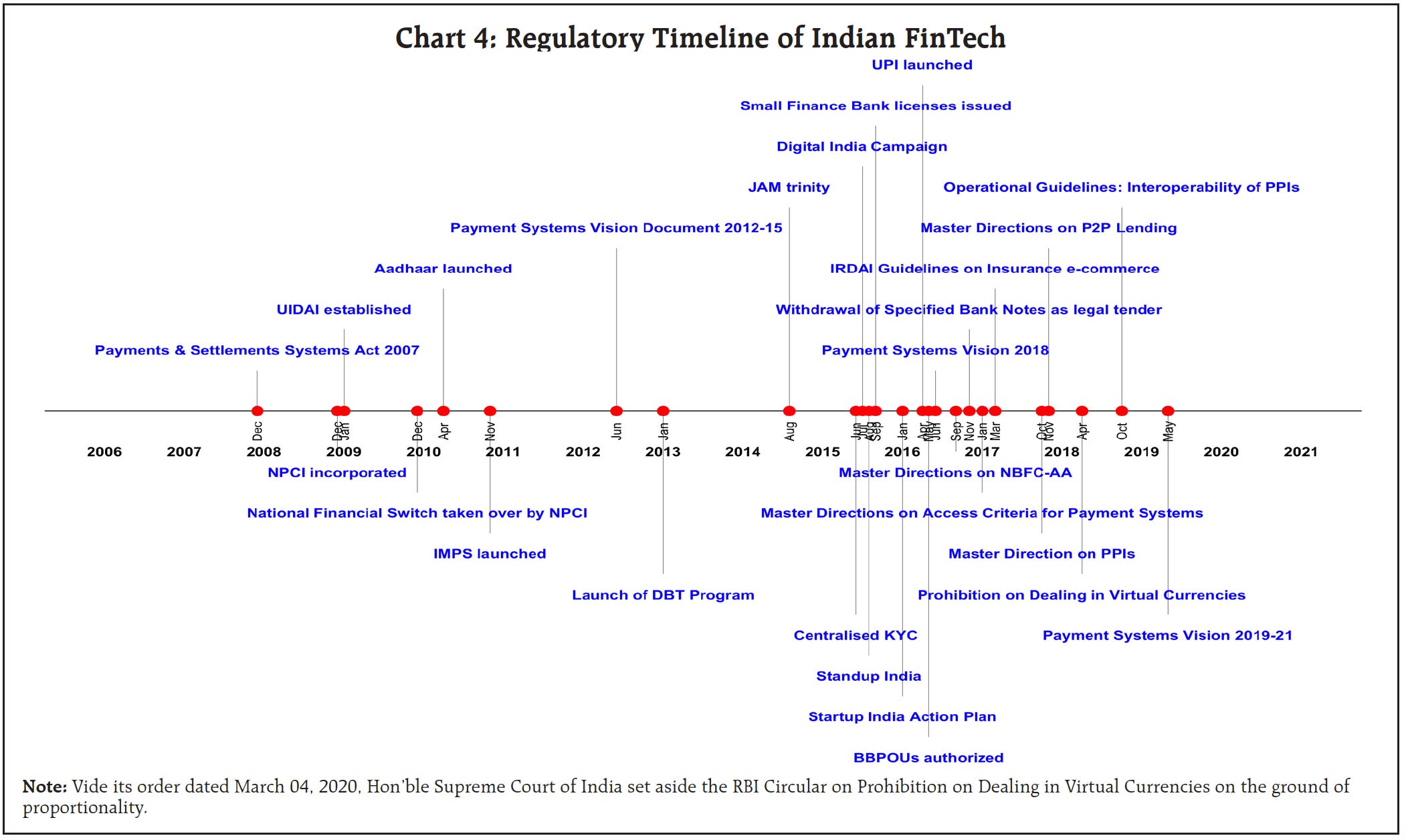

The article highlights that just like India, most countries did not have a separate regulatory regime for everything related to FinTech. However, they did have a couple of rules related to payment systems. That makes sense. When you see the list of FinTechs in the Annex, the top share is cornered by payments and investments.

If you observe regulatory timeline for RBI, you’ll notice that almost every alternate regulation is on Payment Systems in the country.

During the lockdown, retail payments increased at a breakneck speed, especially mobile-based payments (UPI and IMPS) which hasn’t really a seen a single month of negative growth during this time. The speed at which UPI is increasing - the future isn’t far when the value of its transactions crosses that of NEFT. Today, that may be difficult to fathom (especially since the max value of a NEFT tnx is 10 lacs compared to UPI’s 1 lac) - but remember that even IMPS has a limit double that of UPI.

*Note: Although RTGS has the same upper limit as a NEFT txn, the lower limit is 2 lacs, hence the value is unusually high compared to the others.

What does the future hold for FinTech and RBI?

After reading all the challenges, the gaps and the Governor’s comments to media outlets, here is what I expect in the future:

RBI may soon opt for in-house cloud development or partner with other service providers as more and more FinTech completely migrate to cloud computing. (this is actually a leaf out of the book from the US central bank when it visited the Amazon cloud facility last year)

The second round of applications will be considered for the RBI regulatory sandbox (live testing of startups under limited regulations) very soon, possibly next year - the theme could be the space of investments.

Increased focus on cross-border payments and remittances, coupled with financial inclusion (Fino Payments Bank is doing great in this area)

An exclusive FinTech department to take care of every regulation related to this field.

Of course, more regulations in the field of data protection, privacy, customer awareness and tightening of credit standards.

At present, the RBI has placed guidelines and regulations in the domain of P2P lenders, storage of payment data, Account Aggregators and payment aggregators and payment gateways.

The article also has an Annex listing all the payment-related regulations as well. If you’re working in this space or just super interested, I suggest you bookmark the 20-page document. I’ve even highlighted the major areas, in case you do decide to read it in full. Enjoy!

Give me some videsi drama

Way back in Issue #2, I had talked about digital banks in Singapore. Here’s a short recap since most of you must have missed that piece:

Did you know that out of Singapore’s population of 59 lacs, only 2% is unbanked?

()…Still, when their central bank, Monetary Authority of Singapore (MAS) announced its intention to issue 5 digital banking licenses last year, 21 suitors lined up!

And don’t think getting these licenses are easy. Each winner must commit $1 billion for a retail licence; $72.5 million for a wholesale one. Once formed, the digital banks will also have to achieve profitability in five years.

But there’s one key thing to note here that MAS said,

“The new digital bank licenses mark the next chapter in Singapore’s banking liberalization journey. We welcome firms with innovative value propositions to apply for the digital bank licenses, even if they have not yet established a track record in banking.”

Of course, everything got delayed due to covid. Fast forward to today. There are 14 contenders now, down from 21. You can get the full list in this article. It includes some unknown names as well hotshot companies such as Ant (yes, the Chinese company which suspended its IPO recently).

But that’s not the point.

This has extremely interesting evolving story because of two reasons primarily:

Even though Singapore’s unbanked population is quite low and the market is dominated by traditional incumbents such as DBS, the opportunity for South East Asia is immense.

From CIO,

“The World Bank estimates that around 80% of people in Indonesia, the Philippines, and Vietnam, and 30% in Malaysia and Thailand, are unbanked. Myanmar has one of the lowest levels of financial inclusion in Southeast Asia with only 23% of the adult population holding a bank account. This is exacerbated in rural areas, where connectivity is lower and there’s a poor or lacking finance industry presence.”

Singapore is the ideal destination for companies to expand into surrounding markets.

To be successful in this space, you don’t necessarily need to have the financial service pedigree. In today’s internet economy, you can provide value to customers in a lot fo different ways. To make my point, I borrow an excellent infographic from the article I quoted earlier:

Just from this list you can see that Razer is a consumer electronics company (check their gaming collection, it’s pretty cool) with no prior history in financial services. However, it has a wide reach within the youth.

I have already covered the huge opportunities that SMEs, millennial banking and Banking-as-a-service can provide in earlier pieces. If you have been following this newsletter for a while, you’ll be able to connect the dots with as much ease as I do when I read such news.

Let’s hope more enterprising founders try to provide value in different ways to close the financial gaps across the world.

More Bank on Basak...

International

Each week, I try to highlight racial and gender discrimination/upliftment in banking. Tenth, an "unapologetically black" digital neobank is gearing up for launch with the mission of eradicating the wealth gap for Black America. Named for W.E.B. DuBois' book The Talented Tenth, which argued for using the best "negro" minds to educate and lead the Black community for the general uplift of all. Users can also support historically black colleges and universities via a roundup feature.

National

The theme of “digital future” for this week creeps its way into Indian banks as well. HDFC Bank launched a.. wait for it.. “SmartHub Merchant Solutions 3.0”. If you can get over the name - the concept is this - it allows merchants to instantly open current accounts and accept payments on the fly. It’ll also provide VAS like digitising your khata, put collection reminders, manage your inventory, provide billing software - all on one platform. (Sounds a lot like a combination of multiple FinTechs, doesn’t it?). 32% of CC transactions in the country were processed on HDFC swipe machines (already a market leader). Clearly its wants to future-proof this area. Also, when you’re the most trusted brands in the country, convincing new merchants ain’t an uphill task either.

That’s it for this week.

I love feedback. If you want me to cover a particular news, want to get featured, write a guest post or wanna simply say hi, do reach out to me at anirudha@bankonbasak.com. Meanwhile, share this around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. Since the author is employed by a bank, he has consciously chosen not to report any news related to his company to avoid conflicts of interest. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine, thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action.

Thank you for the article Anirudhha. As you pointed out, RBI has released monthly bulletin after 7 years, but I think RBI has been publishing monthly bulletin every month. The same is available in the website for each month. Am I missing something here?