I have been writing about CBDCs (Central Bank Digital Currency) for some time now, especially focusing on China and then Europe. After the customary wait-and-watch strategy typical of our own central bank, we finally have RBI publicly acknowledging the potential and future of CBDCs.

While I strongly recommend reading the full 9 page article by RBI, here’s some context if you are new to this.

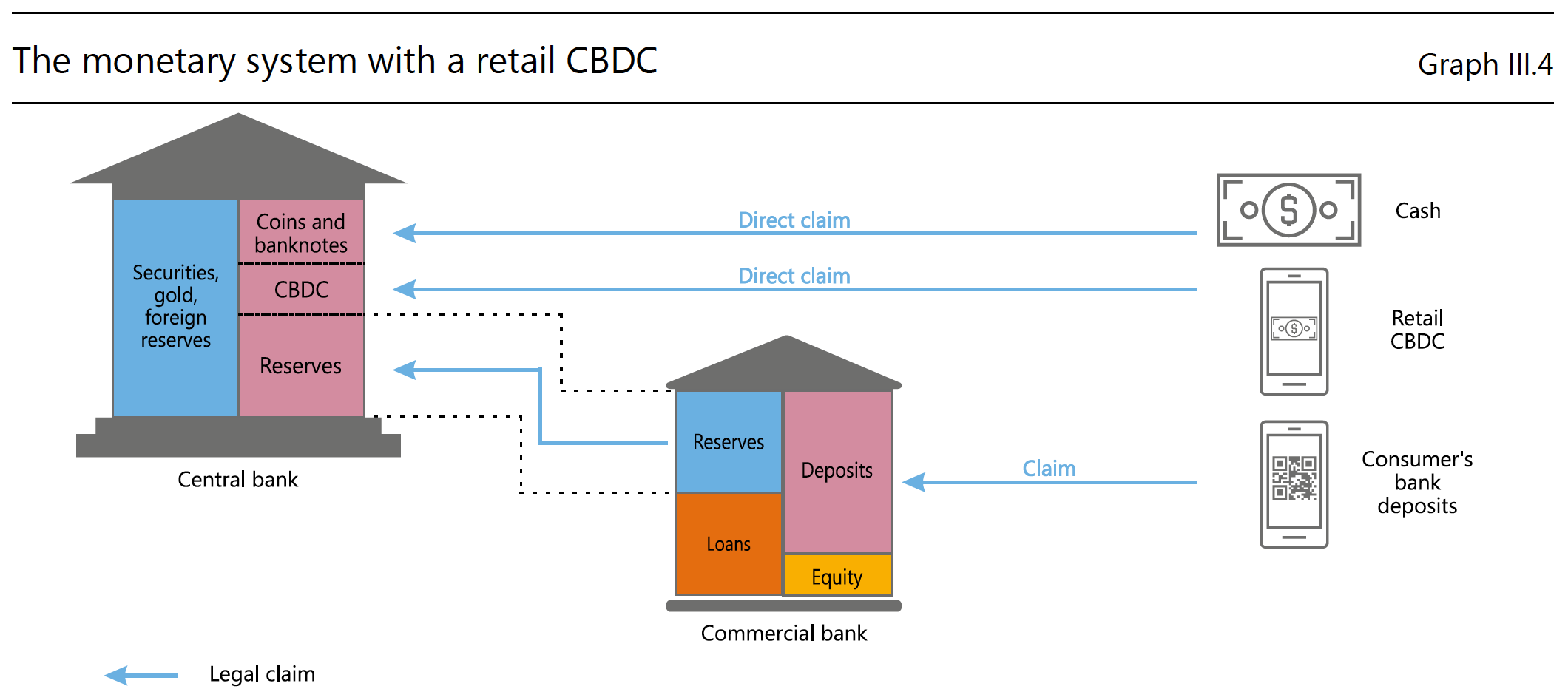

What is CBDC?

To put it very simply, think of CBDC as money. Only the form is different than what you’ve experienced it in since childhood - paper/coins vs digital.

Now the next obvious question is,

We already have digital money, how is CBDC any different?

This question become even more relevant for countries which have fully functional RTP (real-time payments) or FPS (fast payment system) - think TIPS in Euro, Pix in Brazil, CoDi in Mexico, FedNow in US - or - just think of our very own UPI in India!

Thankfully, RBI has addressed this question already. In a survey sponsored by the central bank, it has been found that cash is still predominantly used for paying and receiving money for regular expenses (~50%). Even within this, it is seen that this % keeps increasing as you go down the ticket - High value transactions (above ₹500) are mostly digital, whereas low-value transactions (₹100-₹500) have as high as 70-80% being conducted through cash.

All these numbers might be difficult to grasp for the majority of readers of this newsletter, but India indeed has a unique scenario of:

“increasing proliferation of digital payments in the country coupled with sustained interest in cash usage”

So now the question becomes:

If these people are not using digital payments in the first place, why will they go for CBDC (which is just another digital form of money)?

This question cannot be really answered in a straight-forward manner because RBI’s survey does not reveal WHY people use cash predominantly.

There could be two reasons for it:

People have some form of discomfort towards digital payment

People want anonymity - which only cash provides

CBDC cannot solve for (1) but can definitely solve for (2).

Wait, my UPI transactions aren’t anonymous. How can CBDC be?

Unlike UPI, CBDCs can be configured to be anonymous, so that it doesn’t reveal your identity to third parties (the diagram below offers a good visual explanation of how this will work)

There are of course challenges to anonymous CBDCs which are similar to crypto (what if you lose your private key?) which are still being solved by other countries.

There is another reason why CBDCs have a good case over RTPs like UPI:

Herstatt Risk (or Settlement Risk)

When you transfer money through UPI, there are multiple parties involved - your bank, receiver’s bank (if it is different), RBI, NPCI, the fintech layer/app you are using etc. Although the technology is instantaneous, it is not devoid of settlement risk - the risk of one party not paying the other - in such instances, reconciliation (checking bank records to verify and rectify the transaction) occurs - all this adds up costs.

Imagine you could remove all of this with CBDC. Unlike UPI (which is a technology), CBDC is real money. Unlike UPI, where bank balances get transacted, CBDC can be transacted directly, removing the need for inter-bank settlements.

A related advantage of transacting directly with CBDCs is:

Global Payments

Today, you cannot use UPI to transfer money to USA. However, CBDC makes this possible. RBI goes on to elaborate:

“It is conceivable for an Indian importer to pay its American exporter on a real time basis in digital Dollars, without the need of an intermediary. This transaction would be final, as if cash dollars are handed over.. Time zone difference would no longer matter in currency settlements”

However, this is not as simple as it sounds. Unlike crypto, which is truly global, CBDCs, as the name states, is unique to one central bank. So if Indian CBDC is going to be accepted in USA (or vice versa), both RBI and the Federal Reserve need to figure out the HOW.

This is exactly what Project Inthanon-LionRock is trying to achieve, where the central banks of Hong Kong and Thailand are participating.

This is wonderful! How does it affect banks?

Banks won’t go away, don’t worry.

Let’s take a bank’s basic need to be in the economic system:

Deposits

Loans

CBDCs can remove (1) but not (2). Why? Because the central bank cannot directly lend to you. Banks will continue to be the intermediary.

Additionally, CBDCs replacing deposits is not entirely simple. In order to do that, they need to offer interest, which is not exactly true to its form (Remember we are comparing CBDCs to cash, which also doesn’t provide any interest if you keep it with you).

Got it! So when is RBI going forward with this?

That will take time. A lot of time actually.

This week’s publication is actually the first broad acknowledgement that RBI is even thinking about this. Remember that other countries have worked on this for less than 5 years - you are only hearing about this now because the recent rise of cryptocurrency is actually a threat to fiat money (government issued currency). RBI clearly hates it.

CBDC itself, has multiple options to choose from. A few things which RBI will be considering are:

Should they introduce only retail CBDC (which we just described) or also wholesale CBDC (think of heavyweight financial institutions who directly keep money with RBI)?

Should they use a distributed ledger (think of blockchain) or a centralized ledger (all control with RBI only)?

Should they use token based (anonymous) or account based (identifiable) verification? If they go with the former, how anonymous should the transaction be?

Should RBI directly issue CBDC or allow banks to do it?

Pilot projects considering all these will be started soon, but before that, the RBI Act needs to be modified too. When it was written in 1934, nobody had thought that currency could emerge in any other form.

“Perhaps the time for CBDCs is nigh.”

Finally, what is the state of CBDCs around the world?

To make my job easier, PwC has started publishing the CBDC Global Index from this year, which tracks the progress of each type of CBDC around the world (retail, wholesale, cross-border).

Through this report, I actually discovered that the Bahamas (Sand Dollar) and Cambodia (Project Bakong) are far ahead in their CBDC maturity than China (DC/EP).

That’s all folks!

Considering how important this topic is going to be, I tried to cover the basics first. If you want to go deeper, you can always read all the links embedded in the sources.

As always, share it with someone you think should read up on this.

See you next week! :)

I love feedback. If you want me to cover a particular news, want to get featured, write a guest post or wanna simply say hi, do reach out to me at anirudha@bankonbasak.com or LinkedIN or Twitter. Meanwhile, like this post and share it around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine; thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action.