#29 The Dividend Dilemma

Also, when TLTRO meets ECLGS

The Dividend Dilemma

Why do companies pay dividends?

Among other things, it is an act of “giving back”. A little reward for the shareholders who believed in the company and put money on it.

Banks are companies as well. So there shouldn’t be any discrimination, right?

Apparently not.

From the official RBI announcement,

In view of the COVID-19 related economic shock, it was announced in April 2020 that scheduled commercial banks (SCBs) and cooperative banks shall not make any dividend payouts from profits pertaining to the financial year ended March 31, 2020 until further instructions, which shall be reassessed based on financial results of banks for the quarter ending September 30, 2020. In view of the ongoing stress and the heightened uncertainty on account of COVID-19, it is imperative that banks continue to conserve capital to support the economy and absorb losses, if any. In order to further strengthen the banks’ balance sheets while at the same time supporting lending to the real economy, it has been decided, on a review, that SCBs and cooperative banks shall not make any dividend pay-out from the profits pertaining to financial year 2019-20.

TLDR version of the above statement: “We told you back in April that you can’t give dividends until we decide again in September. Guess what? We decided that you still can’t.”

You might think this is only in India because of our strict regulator.

Nope. Back in March, the European Central Bank had the same concerns.

In fact, almost all central banks had instructed banks to pause dividends for the rest of the year. While some countries (Switzerland, Sweden) have resumed it, others haven’t had the guts to yet.

But why is it such a big deal?

To understand this, we need to go back to the basics.

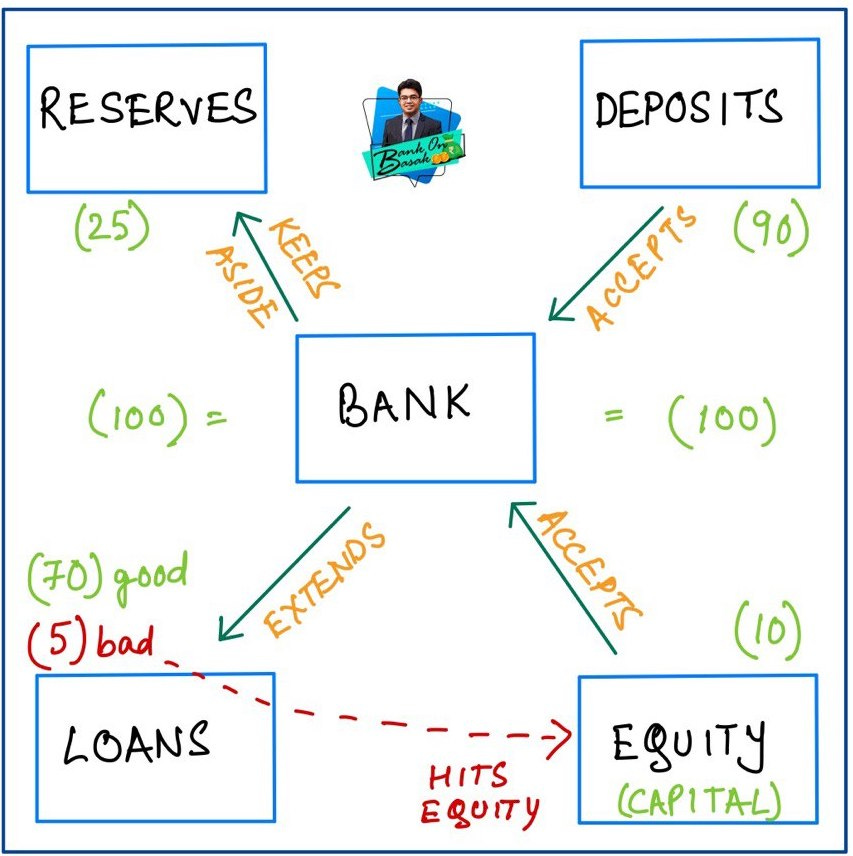

Let’s try to understand the image above. Consider the left and right side to be equal (say, 100), with a bank playing middleman to everything. The figures in brackets beside the boxes are purely indicative.

As you can see, unlike a regular company, a bank conducts it’s business mostly with depositors’ money - people like you and I, who keep our hard-earned money in savings and fixed deposit accounts, for the apparent “safety” that it offers.

So when some of the loans that a bank lends, turn out to be bad or NPAs (and it does - there is no bank with 0 bad loans), the equity capital should act as the buffer (or fall-guy) in this scenario.

All of this is fine when business is running smoothly and you can manage your bad loans. But in a crisis like now, you never know, do you? In the illustration above, what if the bad loans were 15 instead of 5? The equity capital (10) would be completely wiped off - so where is the extra 5 worth of bad loans going to be recouped from? You guessed it - depositors’ money!

To avoid this extreme scenario, regulators want banks to conserve their dividends. Instead of giving it back to shareholders, they can retain the profits and put it back into the capital. More the capital, safer are the deposits!

“Wait, I can be a regular retail investor as well, putting my hard-earned money by investing in the bank through the stock market. Don’t I matter?”

Harsh truth - No.

This is mostly because :

Investors are generally considered more sophisticated than “gullible” depositors.

Unlike depositors who are guaranteed a certain amount of returns on their savings, investors should ideally be prepared to lose their entire money.

Heck, even bondholders of bank are not consulted before their money evaporates into thin air. Remember Yes Bank?

What’s the other side of the argument?

Now that you know why regulators introduce such measures, what do bankers have to say?

Well, think like an investor. Why will you invest in banks knowing that the industry is heavily dependent on the economy, heavily governed by regulations AND the business is tough?

Among other things, it’s mostly a consistent flow of dividends.

When HSBC announced that it would pause dividends to comply with regulations, retail (and institutional) investors were extremely pissed.

Closer home, there are a couple of banks in India who proudly claim that they have never missed a dividend payment in over 100+ years (like City Union Bank which I analysed here).

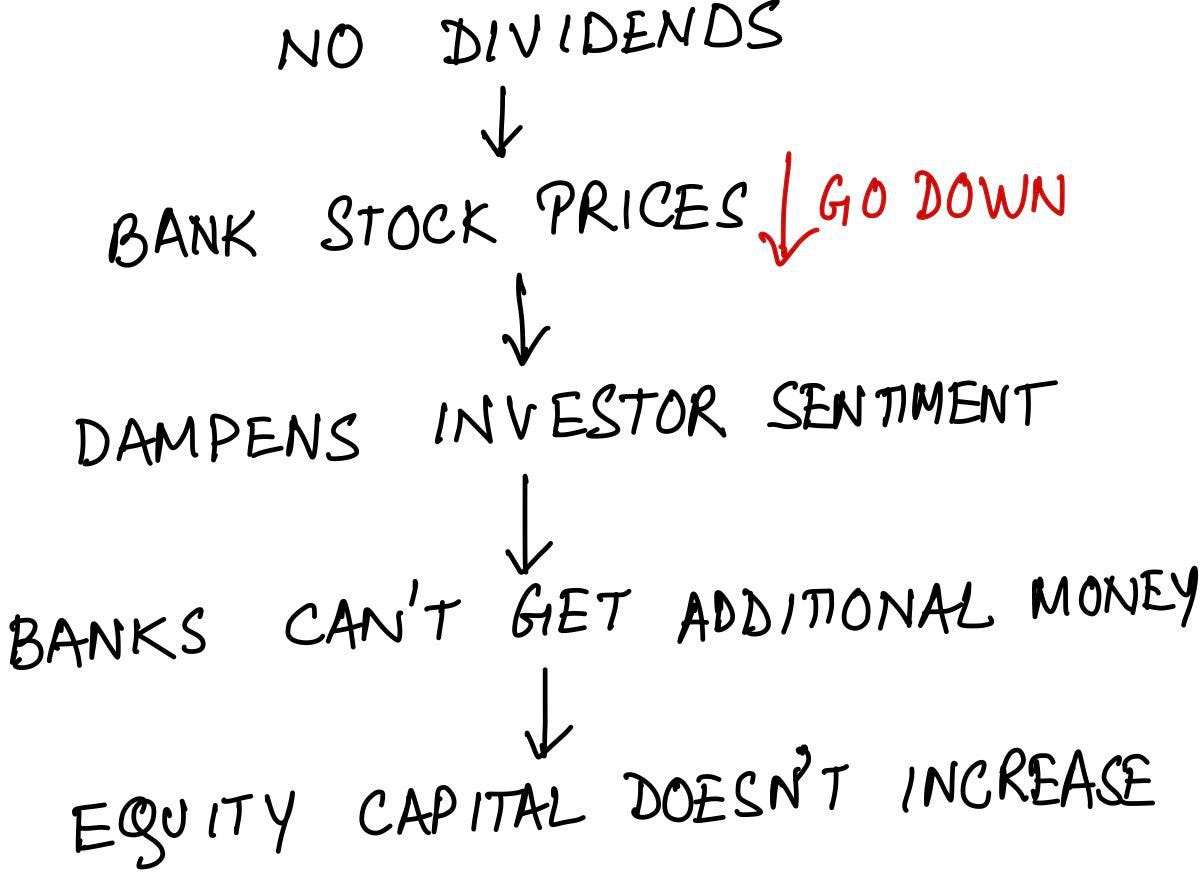

Look, dividend payments aren’t guaranteed. Companies aren’t obliged to give them at all, even when they make profits. But some do. To keep investors happy. So that the next time they come to the markets asking for additional money, investors happily comply.

When you break this cycle i.e. when investors are confirmed that they will not get dividends, like in this case with banks, they not only shy away from pumping in extra money, they even take out the existing investment.

I’ve tried to draw a flow chart to what exactly happens:

Enough of Theory. Give me real-life examples!

The story does not end here.

The lack of dividends affects banks disproportionately.

Consider Kotak for example.

Just like every other bank, Kotak Bank is not supposed to give dividends as well. But RBI went one step further to announce that even PNCP shares won’t receive dividends. Unlike normal shares, PNCP (Perpetual Non-Cumulative Preference) shares offer guaranteed dividends. But if they are not paid for a single year, investors can’t claim it later. No doubts investors are angry.

But is the stock affected?

Nope.

In fact, the bank had no problems raising over ₹7000 CR from the market EVEN AFTER the regulator’s ban on dividends.

Now consider another relatively unknown bank:

Right at the beginning of this story, you might remember that even co-operative banks aren’t allowed to pay dividends.

Now co-op banks function slightly different from traditional banks. For instance, they don’t really have a concept of external equity capital (recall the illustration).

They directly lend out all of depositors’ money. So how does it ensure risk management?

They raise money from the same people they lend the money to!

From RBI’s website,

Let me explain this with an example. Suppose you borrow from a co-op bank. If you borrow ₹100, you also need to buy ₹2.5-₹5 (depending on whether you provide collateral) worth of shares of that bank. Co-op banks keep this money aside as an equity capital.

You don’t mind buying the shares either, since you get dividends on them. You can even transfer them to other investors. Everyone will lap it up since dividends can be as high as 15% in some cases.

Even other banks buy these shares, who’s stocks are in turn bought by credit societies, who’s members are - yup, farmers!

So when you stop dividends, couple of things happen:

New borrowers have no incentive to borrow from these banks. Existing borrowers no longer have a reason to hold back the shares when they return their loans. All of this hurts business.

Farmers (and other rural folks) lose trust in these banks, shying away from deposits, loans and even shares

Co-op banks find difficult in raising external capital, even though rules were changed this year that allowed them to do so. If dividends aren’t paid by ANYONE, won’t I rather put money on a known brand like Kotak?

What do you think?

Now make a call.

I’ve tried to paint a picture highlighting all that actually happens when you stop dividends.

There’s one side which goes “Banks should focus what their core business is! Lending money and not dividend payouts”

There’s the other side which tries to harp the national chord, “What about farmers?”

And then there’s the third, more nuanced, balanced side:

The side which is being enjoyed by NBFCs right now.

Unlike traditional and co-op banks, NBFCs don’t have a blanket ban on dividend payments.

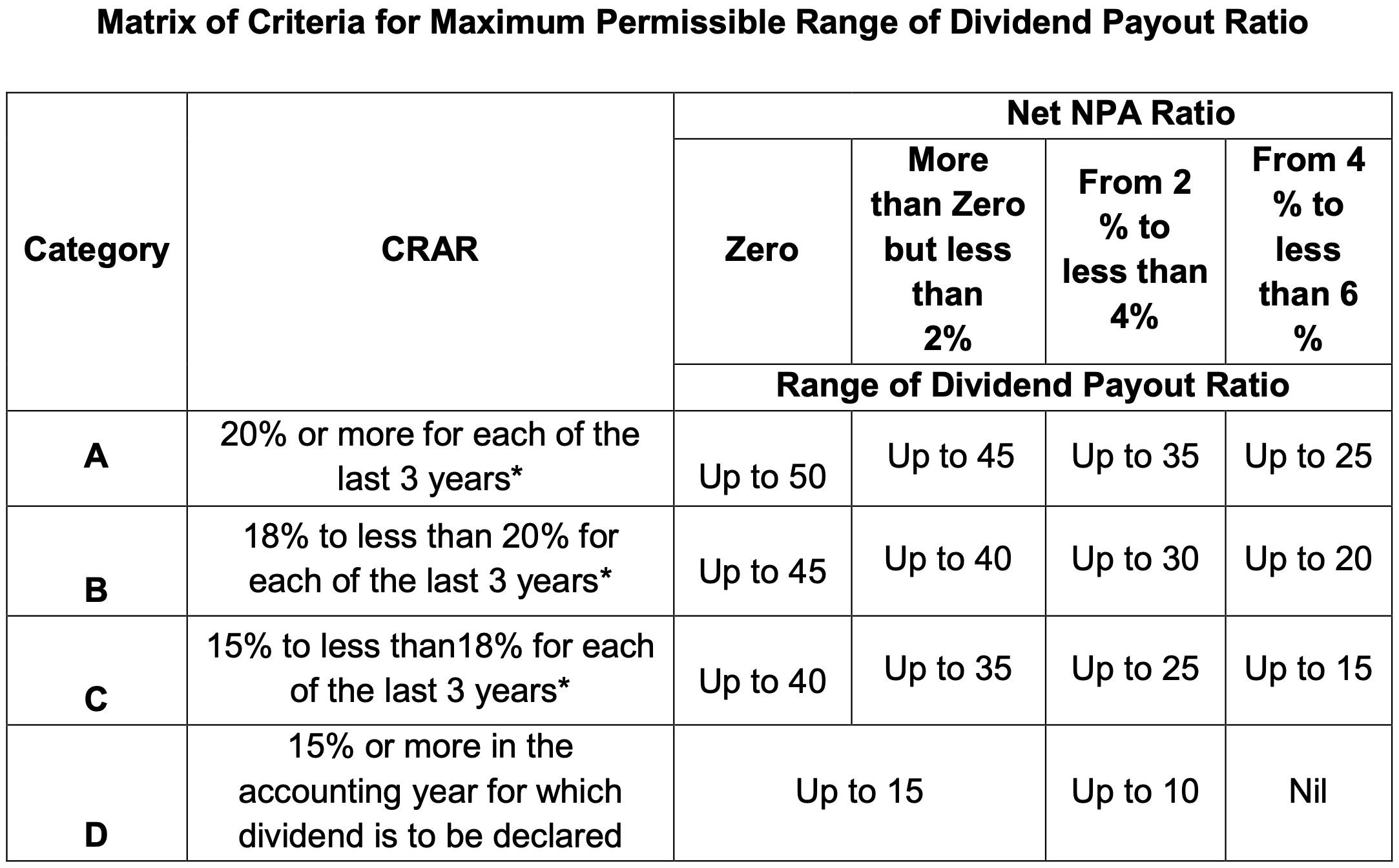

Instead, there are a host of conditions attached to it, all of which are so complicated that they made a matrix to make it simpler (yes, they try):

It basically says that NBFCs are allowed to pay dividends as long as they have a certain minimum equity capital (indicated by CRAR) and a certain minimum bad loans (indicated by Net NPA ratio).

Should banks and co-ops have had such an arrangement as well?

You tell me.

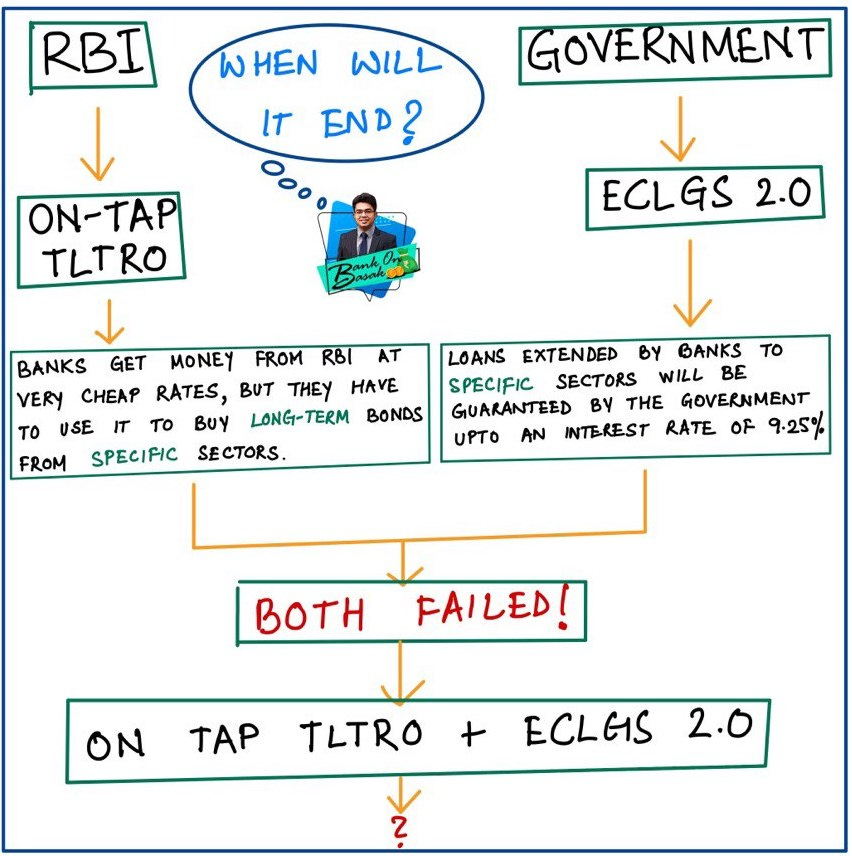

What’s up with RBI?

RBI has extended their On-Tap TLTRO Scheme, in synergy with the credit guarantee available under the Emergency Credit Line Guarantee Scheme (ECLGS 2.0) of the Government.

Lot of big words. Let’s break it down.

As you can understand from the image above, a combination of fiscal policy (by the Government) and monetary policy (by the RBI) was used to nudge banks to lend to sectors which needed the money the most during these trying times. Don’t get me wrong - they made it extremely easy for banks!

Take the concept of TLTRO. You get access to funds at 4% and lend at extremely high rates to justify the risk.

Or ECLGS. Yeah, you can only lend at rates as high as 9.25%; but look at the bright side - even if the loans fail, the government will reimburse you!

But why could the banks only lend to “specific” sectors?

Because the first few iterations of these schemes (TLTRO 1.0, TLTRO 2.0, ECLGS 1.0) were open ended - banks misused the gaps to only lend to high-rated institutions, ignoring those who needed it the most. And you can’t really blame them; when you have to worry about moratoriums, no amount of guarantee and/or cheap funds can incentivise you!

So now RBI is extending TLTRO to the 26 specific sectors that were identified by an external committee back in September.

Did it really fail?

Mostly. Banks have returned the money they had borrowed under TLTRO 1.0 and 2.0 since they found the conditions too stringent to comfortably lend. Moreover, these loans weren't guaranteed.

But ECLGS is guaranteed right?

Yes. But it had problems of it’s own. For instance, borrowers complained that banks were forcing them to use the ECLGS loan to pay back the old loans they had with the bank! Counter-intuitive right? That only helps banks reduce their potential NPAs, but does not increase credit in the system.

Result? Out of a budget of 3 lac crore, only about a half (₹1,58,626; ~53%) has been disbursed till now.

What now?

With each iteration to the original scheme, the government (and RBI) extends the scheme by a few more months, hoping that the full amount gets utilised. This is more to do with saving face rather than actually helping.

Consider this powerful statement for instance:

Banks have been parking excess liquidity of more than ₹6.5 trillion at the central bank’s reverse repo window on a daily basis, which is more than the liquidity of ₹1 trillion made available by the RBI under the on-tap TLTRO.

This essentially means that banks already have enough money (through RBI’s measures + excess deposits that keep flowing in). So the problem is NOT access to funds. The problem are lack of investment avenues and a heightened fear of bad loans. Banks will NOT lend to any sector that they find even remotely risky.

Until the overall economy improves, RBI can simply wait and watch.

That’s it for this week. Sorry had to skip the “Videsi” section due to lack of email space. This always happens when I put a bunch of pictures in the post. But illustrations make these things easier to understand right?

Let me know at anirudha@bankonbasak.com or LinkedIN or Twitter. Meanwhile, like this post and share it around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine, thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice.