If you use social media even sparingly, you’d have realised how grim the situation is across India. Every second tweet on my timeline is people reaching out for help.

If you are in a position to contribute, here are a few ways:

Donate money (to verified links below)

Donate your time (lot of ways to do this - one way is by volunteering to call and verify leads on beds, oxygen, medicines)

Donate plasma (if you are a recovered covid warrior)

Here are two Linktree pages (collection of links) from folks who are collating genuine information - it includes all the things I mentioned above.

Personally, I haven’t been able to either devote time (due to personal and work constraints) or plasma (since I do not qualify). These are the three organisations where I’ve donated equal amounts:

Help Landour Community Hospital to buy a Ventilator& Medical equipment

1:36 PM · Apr 21, 2021

609 Reposts · 523 Likes

My company, apart from donating to similar causes, is also reimbursing the vaccination expenses for me and my immediately family. So I’ll be using that to reimburse someone else’s cost. You can do the same for your household help or any other person in need as well!

If all this is too overwhelming for you, do not worry. You can start by checking in on your immediate friends and family. Some of them might be facing a genuine problem where you can help easily. :)

If you’re one of those who has been remotely affected by this, physically or mentally, please reply to this mail mentioning how I can be of service. I can amplify your covid-related request though my LinkedINor Twitter profile (I am not active on other social media platforms, sorry) - just tag or DM me.

From today (25th April), I’ll be in Kolkata for a few weeks. If you know anybody who needs help locally, I can help with that too!

That’s all folks!

Writing is my own therapy so I’ll continue with the post todaybut forgive me if it’s a little short!

Re-shuffling the Credit Card winners!

In Indian banking, there’s mostly two ways in which you can win:

Lead through product(s), strategy, distribution, competitive rates and all the other ways we talked about here before. OR,

Be on the right side of RBI.

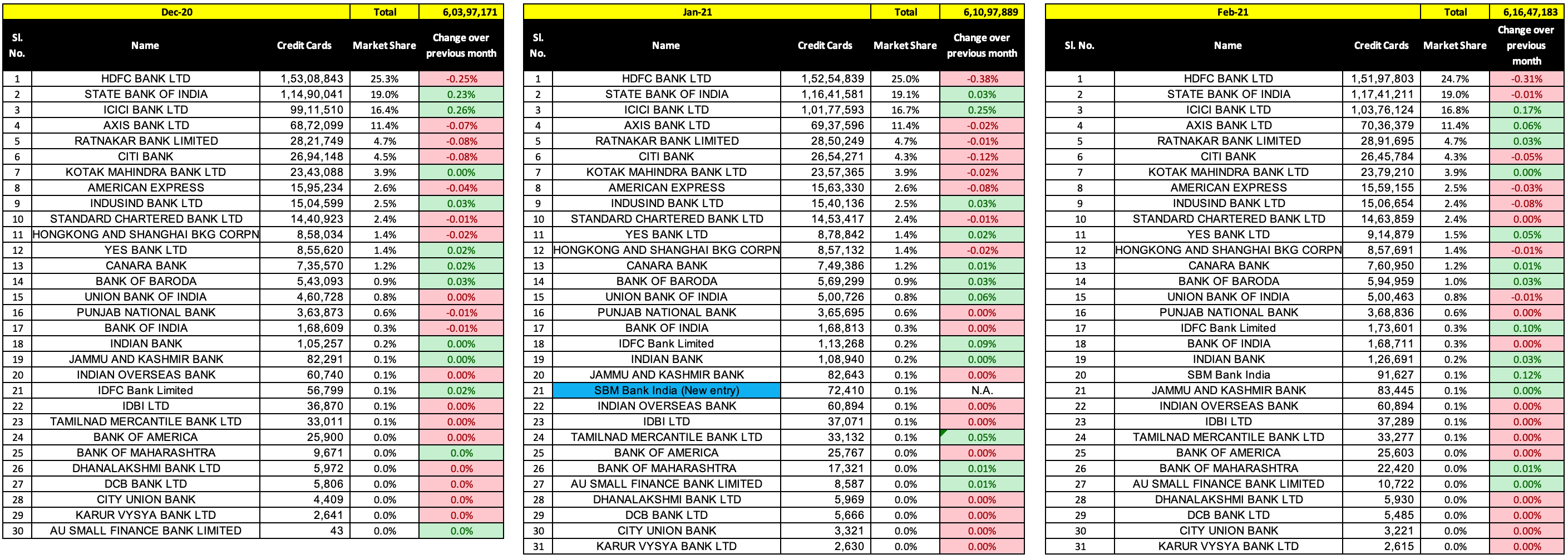

Take HDFC Bank for example. After repeated warnings over its net-banking glitches (since 2018), RBI finally said “Enough is enough” and put a pause to sourcing new credit card customers!

Result?

The bank has been consistently losing market share (an average of 0.3% per month) since December 2020, when RBI came out with the notification.

Who’s gaining at its expense?

If you consider the Top 10 players, almost everyone (except Citi, Amex and IndusInd) have added incremental cards to their portfolio. However, this alone doesn’t guarantee that you’ll gain market share. You need to grow faster than your competition as well.

In that sense, only ICICI Bank has been able to make a meaningful mark here, across the last three months, gaining market share consistently (an average of 0.2% per month).

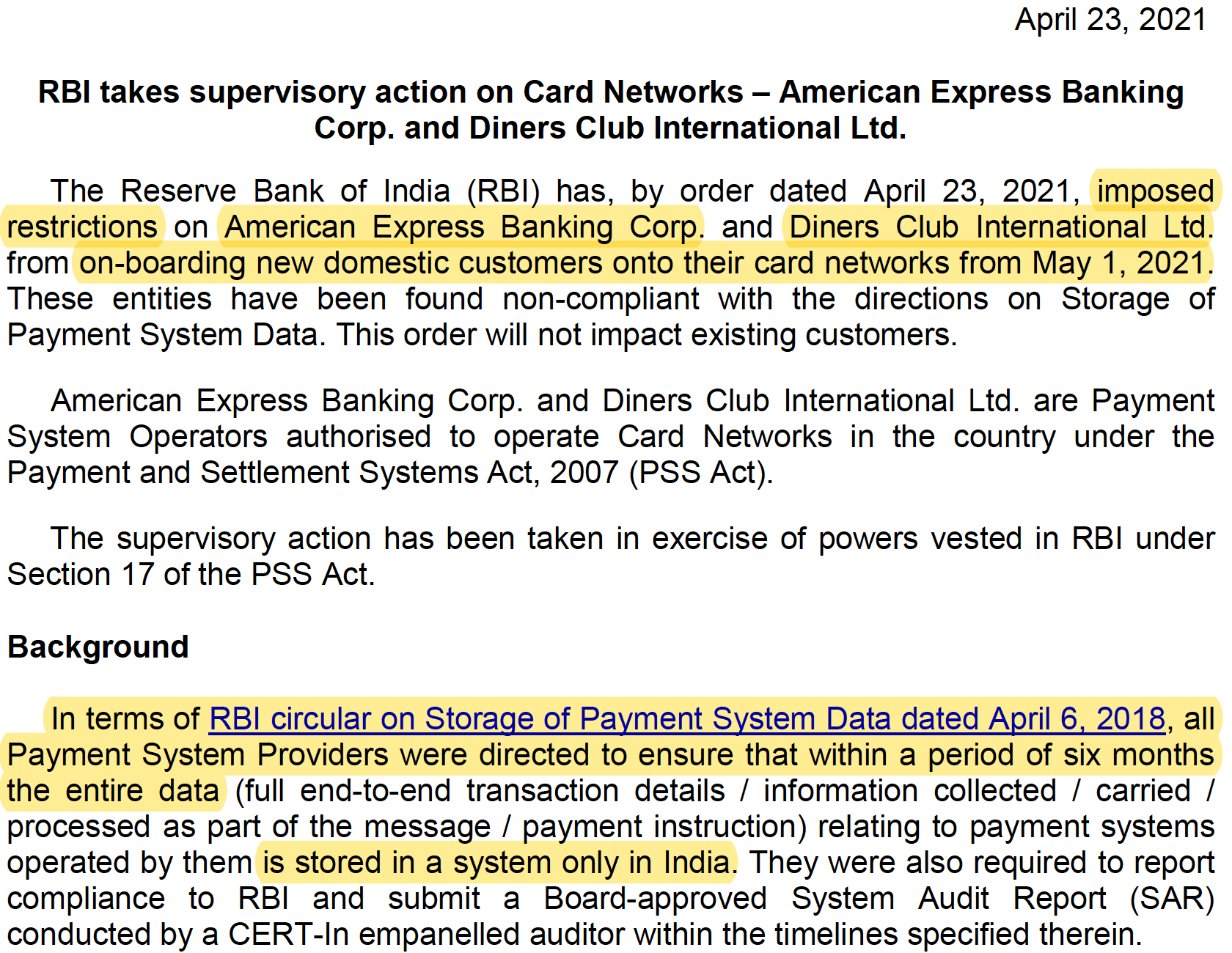

As if other players didn’t learn from this development, RBI has directed another Top 10 player (Amex) from sourcing new Indian customers from 1st May, 2021. Just like in the previous case, this warning dates back to 2018 as well, when RBI came out with a circular instructing Amex to store all transaction-related data exclusively in India.

P.S. Diner’s Club is affected as well. These cards have been operating in India through a tie-up with HDFC Bank since 2011. Both Diner’s Club and Amex are directed towards high net-worth individuals.

With all these developments in credit cards, I became curious enough to manually track the data since November 2020. I thought zooming out to see the bigger picture would help me uncover stuff beyond the Top 10 players.

The Top 10 players have been constant in their ranking for several months now.

Yes Bank is quickly gaining share and may soon find it’s place in the Top 10 (especially if Citi is absorbed by a large player)

Among public banks (except SBI), Bank of Baroda, Canara Bank and Bank of Maharashtra are doing really well.

Among the smaller private banks, IDFC First is gaining share by leaps and bounds (from #21 to #17 in three months)

Among foreign banks beyond the Top 10, Bank of America has been fairly stagnant, HSBC is losing market share but SBM Bank is a new entry (most likely through co-branded RuPay credit cards for MSMEs). In fact, SBM has been partnering with a lot of fintech companies like YAP, EnKash and Finin.

Among small finance banks, AU SFB is the ONLY one issuing credit cards. After launching it for employees last year, it has jumped to 10,000+ cards as on Feb 2021.

For some reason, Central Bank of India dropped off RBI’s database from this year after averaging ~50,000 outstanding credit cards for the most of last year. I couldn’t find any reason for this on public domain, so do let me know if you’re aware! This is especially sad because Central Bank was the first one to launch credit cards in India! It was called the “Central Card”. Neat, right?

I love feedback. If you want me to cover a particular news, want to get featured, write a guest post or wanna simply say hi, do reach out to me at anirudha@bankonbasak.com or LinkedINor Twitter. Meanwhile, like this post and share it around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine; thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action

Did nt know abt Central Card !!