SponsoredGetting an insurance for yourself can be a daunting task.

Unlike a few clicks for a mutual fund SIP or a stock purchase, insurance has multiple types, declarations, options - all this while there’s thousands of advisors waiting to mis-sell you that freakin’ LIC policy.

Behold Ditto Insurance.

From the guys that created Finshots, Ditto Insurance makes the insurance purchase super simple. Their advisory is free, non-spammy, detailed and might I even say, friendly!

Book a call with them today!1

Understanding Navi’s Home Loan Strategy

Home loan demand is back.

Amidst Kotak Mahindra Bank running the lowest home-loan rates (6.5%) during the festive period (September - November 2021) in about a decade, the sector is seeing a great amount of interest from home buyers.

From Kotak’s latest conference call,

“We had our best ever quarter on fresh volumes for both home loan and LAP (loan against property). Like Uday mentioned, we launched a price leadership campaign for a limited period of 6.5%. This has helped us acquire quality customers, strengthen our market share and widen our distribution. This will be a focus area.”

Do you know who’s offering a better price than this?

None other than Navi Finserv, at 6.4%.

It was actually the digital lender’s foray into this segment that got me piqued. When most FinTech digital lending platforms stick to personal loans, why was Navi branching out to home loans?

For the uninitiated, Navi is former Flipkart boss Sachin Bansal’s second venture. According to a recent interview with Moneycontrol, he seemed averse to calling Navi a FinTech company.

“We are now comparing ourselves with banks and NBFCs. That’s why I don’t call ourselves a fintech company. That is why we describe ourselves as a financial services company that happens to be good in technology. I don’t like the word fintech, lot of fintech don’t have their own books… fintech sounds a little less serious”

What does he mean by “lot of fintech don’t have their own books”?

In essence, true fintech digital lenders (without a NBFC license) are not supposed to lend from their own balance sheet anyway. The ones who do, eventually get caught in an ED investigation. ⬇️

Recently, RBI put out a report which listed the number of “illegal” apps in India, which in some form or the other were bypassing regulations.

In such a scenario, having a NBFC or a banking license is a moat. Sachin is aware of what the regulator wants and is careful to choose his words accordingly.

“We are not a neo bank, I think neo banks are a customer funnel for some big banks. That is not a very attractive proposition for us. We are trying to work backwards and see what a bank for a billion people looks like.”

Armed with a NBFC license, Navi’s next ambition is to receive a universal banking license from RBI (Navi has already applied for it early this year under the name “Chaitanya India Fin Credit” - I’ve covered all about banking licensing earlier here)

Back in April, I wrote about Navi’s two key challenges:

Navi has a high target of disbursing ₹4200 crores by March 2022. Retail lending has seen increasing NPAs since Covid. There are ways in which Sachin is trying to mitigate it, such as having an approval rate of 5% compared to industry figures of 10%+ and focusing on high ticket long duration loans to quality borrowers, but everything would boil down to repayments. As of December 2020, gross NPA figures were around 4%, almost fully provisioned.

Navi is trying to diversify Chaitanya’s micro finance-heavy loan book, by expanding into home loans. This segment, although lucrative, is very difficult to leverage technology due to manual onboarding processes (resulting in high costs). More on this later.

As per numbers provided to Moneycontrol, their target is on track.

For someone aspiring for a universal banking license, expansion into home loans will also look good in the regulator’s eyes. If they want to maintain a loan book mix equivalent to their current growth rate (assuming all of the non-microfinance book consists of home loans and LAP), they would need to disburse an additional 900-1100 crores in home loans within the next six months.

For some context, if I take Kotak’s example, it grew its home loan portfolio by ~7000 crore in the same duration (April-September 2021). However, Kotak wouldn’t be the right example.

Let’s take CSB Bank, who’s current Home Loan book (including LAP) is approximately 600 crore, around the same book size as Navi (some reports claim that Navi’s home loan book is only 60 crores).

Unlike Kotak, CSB is not very enthusiastic about this product now. Here are a few snippets from their latest conference call:

“Now considering the inflation, there is a negative return for depositors, which cannot be sustained for a longer period. Deposit rates will go up and at that time if you start raising home loans, defaults will also increase. So this is not the right time to launch home loans. We do have home loan products.”

Why is Kotak Bank bullish on home loans and CSB bearish?

A good understanding of this dichotomy will help us understand Navi’s strategy better.

From reading management commentary, I understood three things affecting home loan strategy:

Cost of Funds

Outsourcing vs In-house

Cross-Sell Opportunities

1. Cost of Funds

This is the cost at which the financial institution is able to raise funds from the market (or customers). For Kotak, that’s freakishly low. CASA (current account and savings account), the cheapest form of funds for a bank, is as high as ~60%. Kotak provides a measly 3.69% on their savings account. Thus, they can afford to launch a price leadership campaign at 6.5% and still afford to make a decent margin. Additionally, this is the rate that they would offer to the highest quality borrowers. Apparently, they’re getting a lot of NTB (new to bank) customers as well - so it’s a growth strategy and its working well. I’ll soon address why NTB customers are important.

For CSB, cost of funds are higher at 4.3%. Additionally, CASA is only 33%, which the bank is trying hard to grow. Thus, CSB offers rates anywhere between 8-9% for home loans. At this higher interest range, they will usually get customers with a higher risk profile (As an example, imagine yourself knocking on Kotak’s doors for a home loan; if you’re rejected for some reason, you’d naturally end up at CSB’s offices). This is evident from the concall. A significant portion of CSB’s NPA come from home loans:

For Navi, their NBFC license wouldn’t be able to attract such low rates that banks can command. It is only Sachin Bansal’s capital infusion that the company is able to launch a price war with leading banks. This may provide some immediate growth, but will definitely be hard to sustain.

Outsourcing

Recall that Navi doesn’t compete on price with personal loans, it competes on experience. Why doesn’t it do the same for home loans?

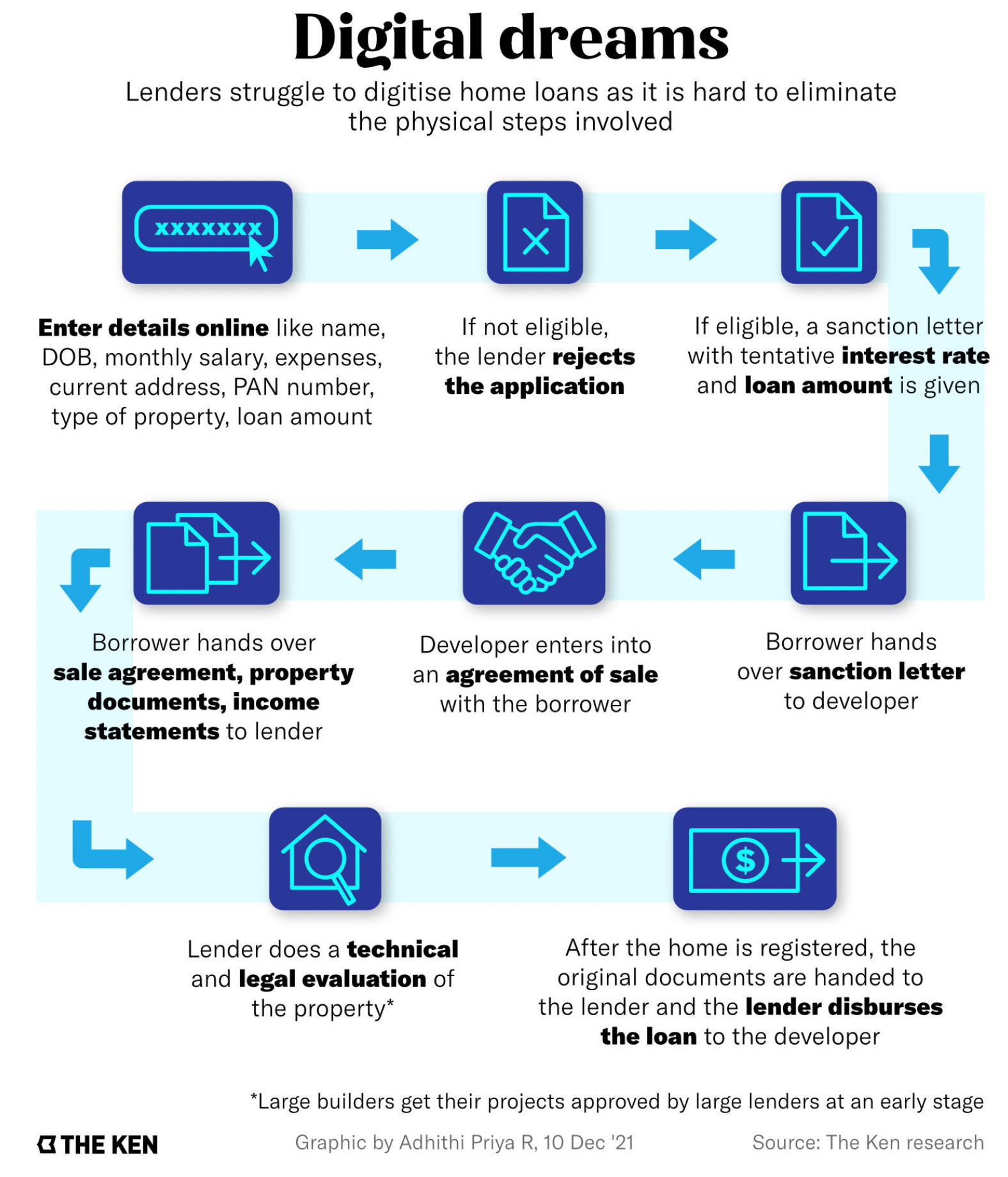

This is because a significant portion of the home loan journey is difficult to bring online. The Ken has made a beautiful infographic to explain this.

Because of the complicated steps involved, very few banks do it completely in-house. Even with Kotak’s prowess, 45% of home loans is outsourced. For smaller banks such as CSB, almost the entire home loan business is handled through HDFC.

“…We are signed up with HDFC Limited, for selling their home loans for the time being. It will help us to streamline our processes and train our people and work along with HDFC to gain enough experience. This will be useful for future when we reduce our cost of deposit substantially by increasing the CASA proportion and are in a position to sell home loans aggressively.” - CSB management

Cracking home loans is tough. Smaller entities usually dip their feet by giving leads to larger players or originating the loan for them.

Just like everyone else, Navi will have a tough time building relationships with developers (usually the place where most deals are closed), attracting customers (through the lowest rates) as well as evaluating customers (same logic holds true here as well - only the top borrowers would receive the 6.4% offer).

Cross-Selling

Here again I would like to quote straight from CSB’s concall,

“The standalone home loan is profitable only when cross selling is very effective. We do not have the entire range of products for cross selling. Once we increase the number of products offered to retail segment and we are good at cross selling, then only we must think of launching home loan on our own on a larger scale.”

Compare this with Kotak’s management:

“Our asset cross-sell in Q2 was strong across retail asset products, led by home loans, LAP…”

As you see, because CSB has a limited number of retail offerings it can offer (compared to Kotak), it doesn’t make sense for CSB to go big on home loans NOW. It can always change its strategy later.

Navi too, doesn’t have a huge retail portfolio to cross-sell now. Existing products such as insurance are primarily push products, while index mutual funds are hardly income-generating.

Remember the importance of NTB customers? Since they do not have products with other existing players, it is easier to sell stuff to them. So an important question to ask is - Is Navi targeting existing or NTB customers?

Out of the three areas that I discovered to be key to home loan strategy, as a reader, you might not seem very convinced of Navi’s growth prospects. Reports mention that while evaluating the next product after personal loans, Navi’s management chose home loans over credit cards. So what’s happening here?

I reckon that a lot of it has to do with the housing market in general. Navi’s presence in South and West is what contributes ~70% of total home loan outstanding.

In terms of volume, Navi’s target segment (above 10 lacs) constitutes almost half the market size (contrary to the popular opinion that affordable housing has a greater pie).

Even in terms of GNPA, larger HFCs (housing finance companies) tend to have lower defaults than medium or small HFCs. Housing finance as an asset class has the lowest annual credit losses amongst all large financial asset classes mainly on account of the collateral and the secured nature of the funding.

Even collections are the best for home loans (along with gold loans)

All of these factors may have convinced Navi to push the bar here. Of course, Sachin is extremely ambitious and may just surprise everyone!

“I think at Navi we are very new, still early but very excited if we are given the opportunity to build a bank by RBI. We will do a tremendous job, of building something completely new that the world has never seen. India is the place for this.” - Sachin Bansal

Other Cool Stuff I’ve Read

More bankers join well-funded FinTechs (link): While reading this, I was surprised that Nilufer Mullanfiroze, who played a crucial role in building the cards and partnership business for Federal Bank. She recently joined as the Head of Banking at a wealth-tech startup. This is a trend that is only going to blow up moving forward. (I remember when I started this newsletter, I had a section titled “Movers and Shakers” which highlighted bankers moving between banks). Almost every FinTech startup, which has operations or sales or requires heavy partnership with traditional banks, would want to hire smart folks with experience. They could help with regulations, building teams as well as contacts.

India's Banking Revolution Has Started Without the Banks (link): Andy Mukherjee elucidates this well in his opinion piece. It draws on Niti Aayog’s discussion paper on digital banking (which I’ll separately cover soon) and highlights the lethargy in the transformation of technological services for one of the world’s most valuable lender - HDFC Bank. Yet, digital giants like PayTM, PhonePe, GPay are held back due to an archaic regulatory regime. When will this change?

That’s it for this week.

P.S. I love feedback. If you want me to cover a particular news, want your brand to get featured, write a guest post or simply want to say hi, do reach out to me at anirudha@bankonbasak.com or LinkedIN or Twitter. Meanwhile, please like this post and share it around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine; thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action.