#26 Indian Banking 2.0

Unpacking RBI's IWG report...

Hey folks! There’s a LOT to unpack this week, just from RBI notifications - so to keep within Gmail length limits, the LVB fiasco will have to take a backseat. :(

Don’t worry, I’ll write a more nuanced piece from a strategic POV when more details emerge from its merger with the Indian subsidiary of Singapore’s DBS Bank Ltd.

In the meantime, here’s an observation - Recently, a lot of you have emailed me with feedback - even if I don’t reply, I read all of them. However, I noticed that most of you don’t click on the “like” button as you’re reading directly from Gmail. If you’re a regular reader and you like what I post, do hit that ♡ symbol right beside my name on top.

Apart from other things, it helps me gauge a sense of non-verbal feedback! 😇

What’s up with RBI?

Of course, the highlight of the week was RBI’s report of the Internal Working Group to Review Extant Ownership Guidelines and Corporate Structure for Indian Private Sector Banks.

If you think the name is long, wait till you read the 100-page long report.

That is why RBI has released a one page summary as well.

Big News #1

Before we dig in, it is important to understand the context. This report was long awaited by a lot of people, especially investors. Here’s a mail I received last month.

P.S. Although I write on this industry, I really am NOT privy to any insider information. I had to wait for the report just like everyone else.

As you can understand from the mail, one of the key recommendations from the report was this,

The cap on promoters’ (owner) stake in long run of 15 years may be raised from the current levels of 15 per cent to 26 per cent of the paid-up voting equity share capital of the bank. This stipulation should be uniform for all types of promoters and would mean that promoters, who have already diluted their holdings to below 26 per cent, will be permitted to raise it to 26 per cent of the paid-up voting equity share capital of the bank.

When I was read this, I couldn’t help think about the tussle between RBI and Uday Kotak (promoter of Kotak Bank). I covered it in detail here but here’s the short version:

In 2013, RBI introduced rules to bring down promoter stake in banks to 15%. However, at that time, Uday Kotak still had roughly 40% stake in the bank. He tried hard, but could only manage it to reduce it to 26%, post which he raged a court battle with the central bank and WON!

At that time, I had contested that it doesn’t really look good if RBI allows only one bank with favourable treatment (In fact, IndusInd Bank promoters had a huge issue with it). Is this move a part of RBI saving its face or does it genuinely believe in higher ownership by promoters?

What is RBI’s logic?

It was also observed that the P. J. Nayak Committee (constituted by Reserve Bank), in 2014, had recommended promoters’ holding of 25 per cent recognizing that low promoters’ shareholding could make banks vulnerable by weakening the alignment between management and shareholders.

However, the authors extensively quote international practices throughout the report. Here’s what I dug up from the Annex:

As you can see, banks in all major economies have diversified shareholding (UK and Germany have limits of 20% and 15% respectively).

P.S. The image below is the current complicated structure for equity ownership in banks.

My take: Instead of going back and forth with these regulations, RBI should focus more on bumping up their tech so that it becomes a faster and more efficient “second set of eyes”. We have bad apples on both sides of the argument - one of the largest private banks in India ran into trouble despite having the most diversified ownership. Similarly, Yes Bank, which had a high promoter shareholding, failed miserably (and is desperately trying to get back up). 15%, 20% or 26% - just make up your mind and move on already.

Big News #2

Large corporate/industrial houses may be permitted to promote banks only after necessary amendments to the Banking Regulations Act, 1949 to deal with connected lending and exposures between the banks and other financial and non-financial group entities

Big News #3

Well run large NBFCs, with an asset size of ₹50,000 crore and above, including those which are owned by a corporate house, may be permitted to convert to banks provided they have completed 10 years of operations and meet the due diligence criterion and satisfy certain conditions

Let me unpack these together. Here’s a tweet to set the context:

For the uninitiated, Sanjiv Bajaj is the CMD of Bajaj Finserv, an NBFC, which in all likelihood, meets the criteria to turn itself into a bank. However, don’t let the tweet mislead you.

Las year, Sanjiv categorically said this,

Why the change of heart?

I don’t follow NBFCs as closely as banks, but here’s a few pros and cons of these recommendations:

The banking scene is definitely going to get a lot hotter. Personally, I love competition. When Private Banks came into the scene, public banks didn't really bother because they’re…well, public banks! However, private banks have a lot MORE to lose. Some of them are so big that they can even get away with hidden charges which you don’t really find in public banks.

You’ll often hear that “cost of funds” for a bank is a lot less than NBFCs - here’s what it means - any lending institution first needs access to deposits. A bank can pay people like us to keep money at throwaway rates (~3% for savings account, ~5% for term deposits and practically 0% for current accounts); however, an NBFC is not allowed to accept deposits from the public; thus they need to pay a higher interest to whoever they’re borrowing from (it’s mostly banks).

A definite con that comes along with a banking license is the increased scrutiny by the central bank.

In a recent speech by the Deputy Governor, it was highlighted that between March 31, 2009 and March 31, 2019, the total assets of NBFCs grew at a compounded annual growth rate (CAGR) of 18.6%, while the balance sheets of scheduled commercial banks (SCBs) grew at a CAGR of 10.7%.

Clearly, you can grow faster when there are lesser eyes on you. From the same interview, I quote Sanjiv Bajaj again,

“Finance have demonstrated over the last 10-11 years that you do not need a bank licence to do 70 per cent of what a bank does”

The only reason that corporates and industrial houses HAVEN’T been allowed to promote banks is because of obvious conflict of interest issues. What if the corporate diverts money, gained through deposits from gullible retail investors like us, to loan its own business groups? We ALREADY have instances such as these without the rule - so if this does pass, RBI will have to divert more focus and energy to scrutinise them.

My take: Through different editions, I have made it clear about my long-term wish from this industry - more (and better) financial access. I don’t believe these changes align with that. The biggest NBFCs (you can check this filter on Tijori to see which of the NBFCs qualify) do not really have a problem when it comes to access to funds. It’s the small ones that do - who are actually trying to make a difference, with last-mile connectivity. When do they get their due attention?

Also, I highlighted in my last post how Singapore’s digital banks are vying for a license by showcasing what value they can bring to the table. We have a long way to go in India before a corporate shows that sophistication while asking for a license. Or maybe the incentives from the regulator are not enough?

Other News

It seems that the working group has recommended a much-needed relaxation in stock listing requirements for payment and small finance banks. From the report,

By end of September 2020, out of 22 universal banks in the private sector, 20 are listed and two (Tamilnad Mercantile Bank and Nainital Bank) are yet to be listed. Out of 10 Small Finance Banks (SFBs), two are listed (AU SFB and Ujjivan SFB). No Local Area Banks and Payment Banks (PBs) is listed so far.

Although rules were changed for universal banks to allow them 6 years before they needed to list, SFBs and PBs had only three years to list once they reached a net-worth of ₹500 cr. This is a really short time, especially in a sector involving money (and consequentially, trust). Should a bank focus on building operations or building trust within such a short period? Keeping this in mind, it has been recommended that they get 6 years breathing space as well.

But wait! What if these banks cook up their books to show a net-worth below ₹500 cr to delay their listing? (remember, IPOs mean more disclosure and transparency)

This is why the report ALSO recommends that these banks should mandatorily list within 10 years from the date they begin operations (just in case they don’t meet the first criteria).

We already have so many SFBs lined up for an IPO. And by 2027, we can expect to see Airtel, PayTM, Jio, Fino (much-awaited), IPPB, NSDL Jiffy - all of their payment banks list in the stock markets as well (if they survive till then).

As always, RBI has allowed about two months to invite comments on this report through this email ID - ogcsfeedback@rbi.org.in. It is important to remember even though the report is by an internal group, they are still… recommendations. We will have to wait another couple of months before the final rules kick in.

More RBI Notifications…

#1

With all the noise from the IWG report, a very interesting piece of development got ignored.

If you remember my August 6 coverage on RBI announcements, the central bank wanted to set up an Innovation Hub to support and promote new technology in areas such as cyber-security, data analytics, delivery platforms and payment services all for the purpose of attaining financial inclusion and more efficient banking services.

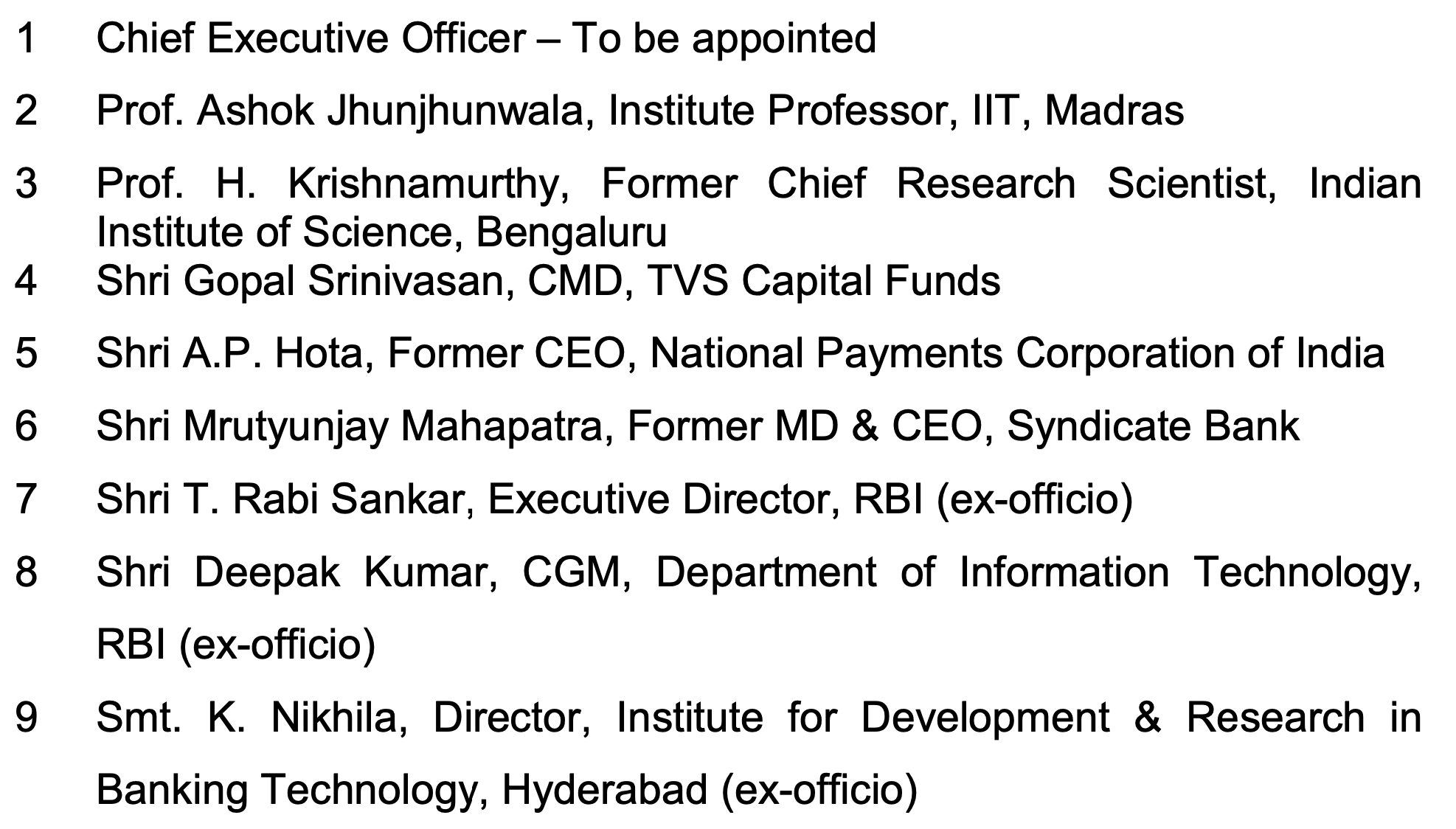

Well, we finally have that, to be headed by the great Kris Gopalakrishnan, co-founder and former co-Chairman of Infosys. Here are the other members:

That’s certainly a nice empty CEO hot seat.

#2

I had also mentioned about a regulatory sandbox (controlled environment with relaxed rules) that RBI had set up last year, which got a backseat due to C-19. We have the first cohort live now. Out of a whopping 32 entities, only six have been selected for the ‘Test Phase’. The central bank has released the details of the first two:

I absolutely love both these entries as they go with the theme of financial inclusion. When we talk about the mammoth growth of UPI, we often forget that it requires a smartphone for it to work, something that a considerably large chunk of India DOES NOT have access to. Do they not deserve financial access?

Offline payment products have seen huge innovation recently. I had recently contributed an article for GoMedici, where I talked about three more companies in this exact space.

Can’t wait to read about the other four startups!

That’s it for this week.

I love feedback. If you want me to cover a particular news, want to get featured, write a guest post or wanna simply say hi, do reach out to me at anirudha@bankonbasak.com. Meanwhile, share this around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. Since the author is employed by a bank, he has consciously chosen not to report any news related to his company to avoid conflicts of interest. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine, thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action.