#44 Digital Change!

PPIs + MPC Report

Hey there!

Before we jump in, here’s a word from our sponsors:

Do you want a savings account which can double up as your wealth account as well? Niyo X offers you the convenience of both. Once you open an account, you will not only get the benefits of earning some extra interest (up to 7%) and a virtual debit card for immediate use, but also start investing in mutual funds (at 0% commissions) right from the same app. No need for two separate apps anymore!1

Payment Banks and Wallets get a new life!

RBI has been complaining about Payment Banks (PB) for a long time now. They’ve highlighted, time and again, how the business model of PBs have been impacted by their inability to lend and a low-interest rate environment (this essentially means that PBs do not earn much interest margin on the funds you keep in their wallets/accounts).

All that said, RBI hasn’t really done anything to help them out, regulation-wise. In fact, you could say that the central bank had made it worse for them, by introducing full KYC norms - the primary reason for slowing down their growth.

After several years, RBI is trying to introduce baby steps for these PPI (prepaid payment instruments), which it thinks might help.

Note about PPI: For ease of understanding, some common PPIs are Amazon Pay, Ola Money, MobiKwik wallet. The full list can be found here. If you do not find Airtel, PayTM and the likes, that is because they had converted into a Payment Bank, yet retaining their PPI license. So for all purposes, when I refer PPI, that includes all these players.

PPIs can now hold balances upto ₹2 lacs (from an earlier limit of ₹1 lac)

You can withdraw cash from these PPIs from your local ATM. This was earlier only allowed for bank PPIs (full list here - includes Payment Banks as well). Now the regulation has been extended to non-bank PPIs as well.

You can now transfer money from one wallet to another wallet (this was earlier voluntary for PPIs, now it is mandatory)

PPIs now have direct membership to RBI operated Centralised Payment Systems such as NEFT and RTGS (earlier only restricted to banks)

Let’s try to unravel all these one by one now.

Increased balances

Impact: Neutral.

Reason: Some Payment Banks like Fino already have a feature where they offer auto-sweep in facility, under which, if users exceeded the wallet limit of ₹1 lac, the extra amount will be transferred to the partnered scheduled bank.

Also, most people do not keep so much money lying around in their savings account, unless the rates are high. For example, Fino users keep an average of ₹45,000. However, traders do tend to keep more, based on their requirements.

Positive: The higher limit does create a perception of increased trust among customers, who might be more willing to keep their money here now.

Withdrawals

Impact: Neutral to Negative.

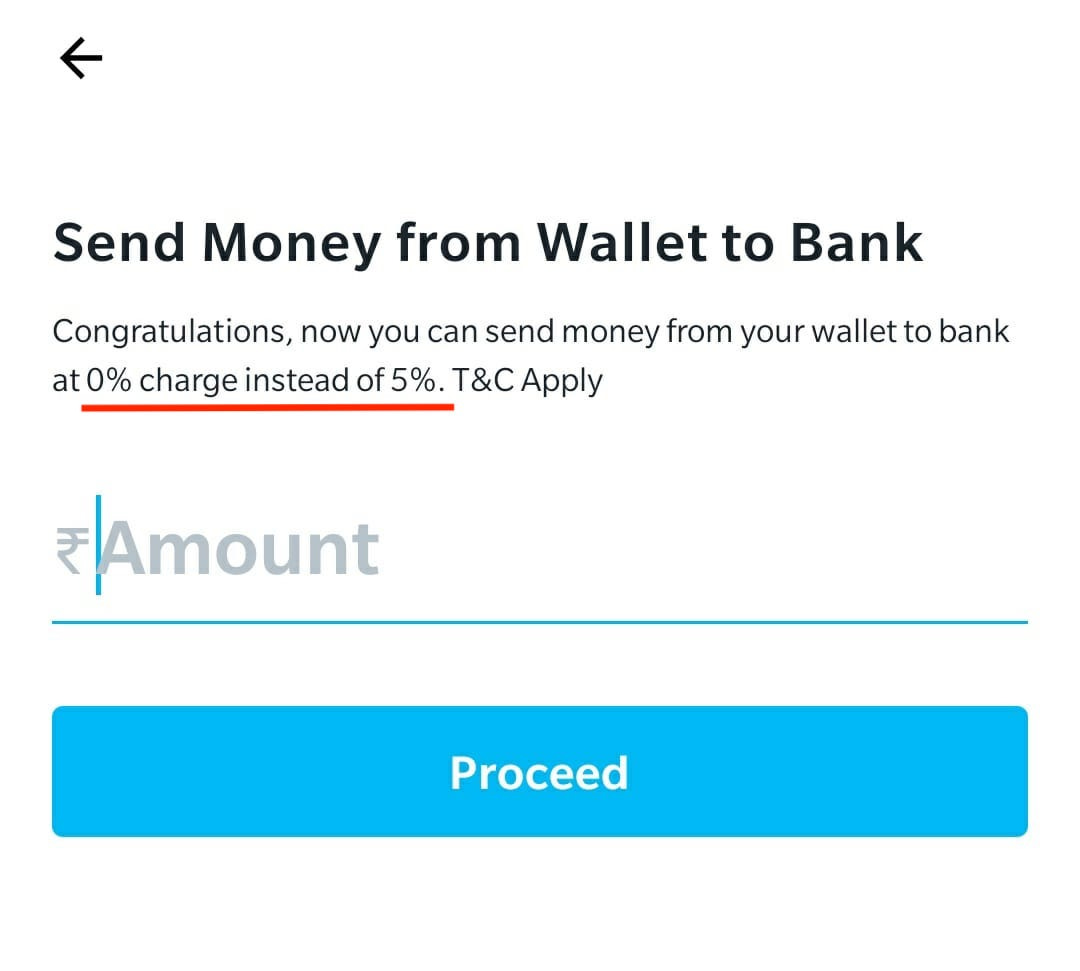

Reason: To understand why cash withdrawals from PPIs could be potentially negative, we have to first understand their ecosystem. Payment Banks like PayTM had seen a massive adoption in its wallet services because of its wide acceptance and cashbacks, which makes sense in a closed-loop ecosystem. You could only transfer money from your PayTM wallet to another PayTM wallet free of cost. If you tried to transfer it to a bank, you would have to pay a convenience fee of 5%. Without the fee, almost everyone would have transferred the cashbacks back to their accounts instead of using it within the platform.

Today, if you go to your PayTM wallet and click on “Send Money to Bank”, you will see this:

Apply the same concept to ATM withdrawals. If you could withdraw the cashbacks so easily, will PayTM incentivise or disincentives users to use the ATM services? Or will it simply stop offering cashbacks altogether? What do you think?

Here’s what Airtel is doing:

Airtel Payments Bank is continuing to offer cashbacks, provided you upgrade the PB account to a complete digital savings account (the CEO is referring to it as a neobank). Of course, in order to compensate for the losses that would arise due to cashbacks, it is trying to lock in the customer with an annual fee (₹299).

Possible use case: Students (under the age of 18) might not have to go through the hassle of opening a bank account anymore. Parents can directly transfer money to their children's wallets and and they can easily withdraw it out of the nearest ATM.

Interoperability

Impact: Negative

Reason: Interoperability refers to the ability to transfer balances from one wallet to another. This feature, along with cash withdrawals, is being pushed by RBI to increase PPI usage in Tier III to Tier VI towns.

However, with UPI itself being interoperable, does it even matter? Wallet interoperability suffers from the same drawbacks as cash withdrawals as well.

In fact, now that it will no longer be a closed system anymore, PPI players might have to increase their security to prevent frauds!

CPS Membership

Impact: Positive

Reason: CPS, or Centralised Payment Systems, refers to RBI operated systems such as NEFT and RTGS. Till today, their exclusive access was granted only to banks. It has now been extended to PPIs as well (including other entities).

Now, PBs and wallets do not have to rely on banks anymore in order to process these transactions. UPI transfers are limited to ₹1 lac only. With RTGS and NEFT now enabled, these players will not have transfer limits as well. Expect faster processing times!

Overall Impact

Although industry players are cheering as digital players inch closer to a level playing field with traditional banks, let us not forget WHY the central bank have enabled these measures. Despite multiple attempts through different strategies, RBI has realised that it is extremely difficult to push for financial inclusion through traditional banks. Even Small Finance Banks, which were made for this purpose, have not done a great job. Will PPI be the flagbearer? Or has RBI’s myriad regulation stumped them since the start?

Now that we know the central bank has started trusting these players a bit more, RBI can definitely take additional measures to increase awareness about them through various campaigns. If you want last-mile connectivity, you gotta take last-mile measures as well!

What’s up with RBI?

I’ve previously written about RBI’s Monetary Policy (MPC) here and here. If you’re already aware of the background, you should know that RBI has released the calendar for the next set of meetings for FY2021-22:

Two major things that you do need to keep in mind though:

On 31st March 2021, our Government (who decides the inflation band), renewed the policy for keeping inflation in the same range of 2% to 6%, for another 5 years. The MPC was first set up in 2016 with an initial validity till March 2021. Considering its success in tempering inflation, this was kind of expected. Here’s RBI explaining the effectiveness:

“From the time after the Monetary Policy Committee (MPC) was constituted in September 2016, average CPI inflation for the period October 2016 to February 2020 – prior to the onset of the COVID-19 pandemic – was 3.8 per cent, down from the average of 7.3 per cent during January 2012 to September 2016”

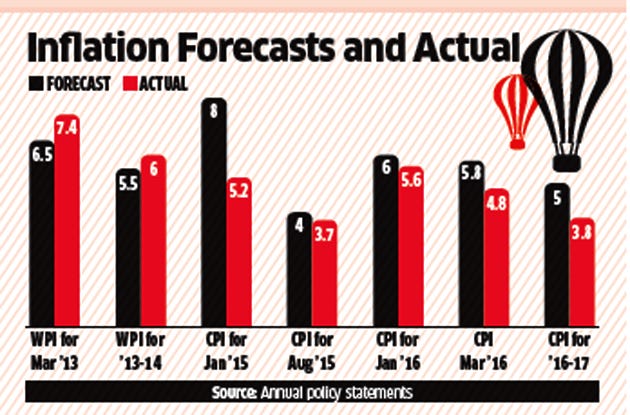

Apart from setting the repo rate (which is the main highlight of these MPC meetings), RBI is also supposed to predict the inflation for the next couple of quarters. However, it has always received flak for not doing a good job at it. Most of the times, it is way off the mark (picture below). So now, it has finally amended the model. Let’s hope for better predictions for the next meetings!

P.S. I’m currently loving the secondary Twitter handle of RBI (@RBIsays) which is doing a great job highlighting the important stuff from MPC, circumventing the need to read the plain old black and white text.

I love feedback. If you want me to cover a particular news, want to get featured, write a guest post or wanna simply say hi, do reach out to me at anirudha@bankonbasak.com or LinkedIN or Twitter. Meanwhile, like this post and share it around?

All views and opinions shared in this article and throughout this blog solely represent that of the author and not his employer. All information shared here will contain source links to establish that the author is not sharing any material non-public information to his readers. His opinion or remarks on any news are based on the assumption that the source is genuine; thus he is not liable for any information that may turn out to be incorrect. This blog is purely for educational purposes and no part of it should be treated as investment advice. Using any portion of the article without context and proper authorisation will ensue legal action.

Disclaimer: Investments are subject to market risk. “Bank on Basak” is not a registered investment advisor and is not associated with Niyo in any form.